Goodcover’s Insurance for Electronics and Wearable Technology: Everything You Need To Know

21 Dec 2022 • 6 min read

Do you own an Apple Watch or another pricey wearable tech but worry about what happens in case of loss, theft, accidental damage, or breakdown?

Don’t fret. Our guide will explain everything you need to know about safeguarding your valuable wearable electronic gadgets without breaking the bank.

Here, we'll discuss how insurance for electronic devices works and what protection plans are available. We’ll also let you know how to leverage your renters insurance policy to cover your portable electronic devices.

Keep reading to learn:

- The Difference Between Insurance for Electronic Devices and an Extended Warranty

- Is an Extended Warranty Worth It?

- Does Renters Insurance Cover Electronics?

- How To Get Insurance Coverage for Wearable Electronic Devices Under Renters Insurance

- Actual Value vs. Retail Value: Which One Does Goodcover Offer?

- Other Advantages of Electronics Insurance With a Goodcover Renters Insurance Policy

- Should You Get Additional Coverage for Your Wearable Tech and Other Electronic Devices?

- Final Thoughts: A Complete Guide to Insurance for Electronics With Goodcover

The Difference Between Insurance for Electronic Devices and an Extended Warranty

Insurance for Electronic Devices

Electronics insurance offers repair or replacement costs for damaged, lost, malfunctioning, or stolen electronic devices. Those include laptops, smartphones, and wearable gadgets.

The repair or replacement cost you'll receive is the maximum insured by your electronics insurance policy.

Extended Warranty

A high-value electronic device usually has a manufacturer warranty or guarantee. Yet both have a limited scope and duration.

An extended warranty is the additional coverage or protection plan you can buy for high-value electronic devices. Examples include wearable gadgets, mobile devices, and laptops.

It will protect against accidental damage or loss longer than the manufacturer’s warranty. And it also offers broader coverage.

For example, your new Apple Watch might have a limited manufacturer’s warranty for mechanical or battery failure issues. An extended warranty would cover problems like a cracked screen (accidental damage). Plus, it would cover misplacement.

Is an Extended Warranty Worth It?

An extended warranty isn’t always worth your money. That’s because it’s more of a service contract. Optional coverage could be denied if you break certain terms and conditions.

Case in point: Consumer Reports called extended warranties “money down the drain.”

Buying an extended warranty might not be the best idea because:

- Manufacturers should offer you at least a 90-day warranty. Paying for an extended warranty for the same period is paying extra for no reason.

- An extended warranty incentivizes manufacturers to shorten their own “express warranties.”

- You can bundle your electronics insurance with your renters insurance. So there’s really no need to pay extra for extended warranties or one-off insurance coverages.

Does Renters Insurance Cover Electronics?

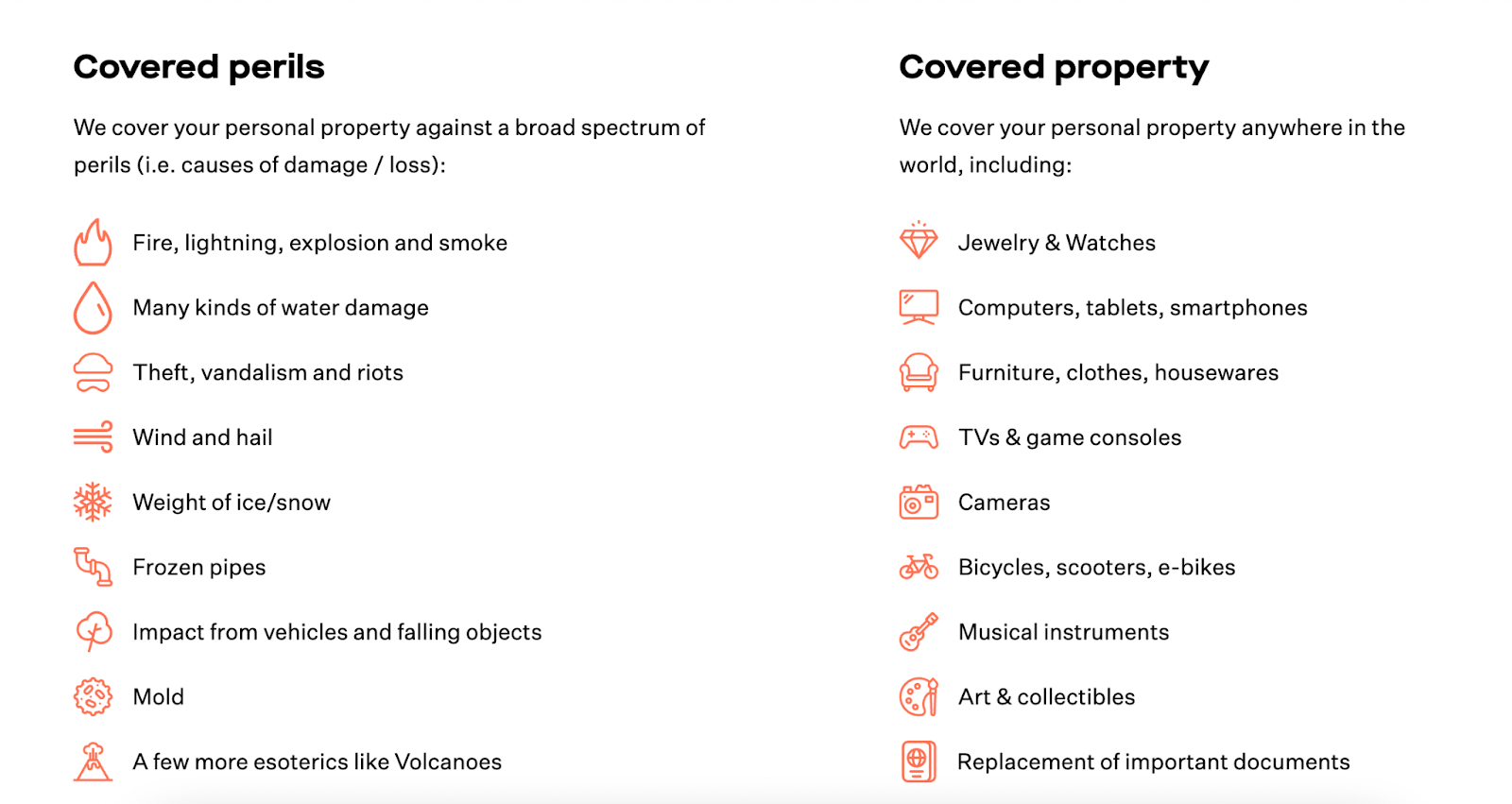

Yes, the personal property section of Goodcover’s renters insurance policy covers electronic devices and wearable gadgets. It protects your personal property against covered perils such as fire, smoke, theft, and vandalism. With our SUPERGOOD plan, accidental damage is covered as well.

How To Get Insurance Coverage for Wearable Electronic Devices Under Renters Insurance

Wearable electronic devices include gadgets like:

- Smartwatches (such as Apple Watch)

- Smart jewelry (such as Circular Smart Ring)

- Fitness trackers (such as Garmin)

Your renters insurance protects your wearable gadgets against covered perils with standard coverage. And with SUPERGOOD extended coverage, your electronic device will also be covered from accidental damage.

Covered perils are causes for damage or loss that your policy covers. They include:

- Fire

- Lightning

- Theft

- Vandalism

- Many types of water damage

- Certain types of mold

- Wind/hail

You don’t need to inform your insurance provider to receive device insurance when buying portable electronic gadgets. Your renters insurance policy automatically covers them as part of your personal property coverage.

That’s also true for devices like digital cameras, desktop computers, iPhones, iPads, cell phones, and gaming systems.

Your policy will state the exact amount you’d receive if your wearable gadgets are stolen or damaged.

Renters insurance policies classify wearable electronic devices under jewelry. They usually have a limit of $1,500 for theft unless you schedule the item for extended coverage. More on that in just a bit.

Actual Value vs. Retail Value: Which One Does Goodcover Offer?

When you file a claim for your damaged or lost wearable gadget, the insurance provider can pay the item’s actual cash value (ACV) or replacement value (RCV).

The ACV is an item’s reduced cost after depreciation. In other words, it’s the price you'd get if you tried to sell your used gadget today.

The RCV is an item’s replacement cost without subtracting depreciation. At Goodcover, we also use the term "retail cost" — the dollar amount it would cost to buy the gadget today at its retail price.

Suppose you bought an Apple Watch for $800 two years ago. Recently, it got stolen while you were shopping in a crowded mall.

If your device insurance plan only covers ACV, the reimbursed amount would be much lower than $800 — maybe around $500.

But if your plan covers the RCV, it might reimburse you $800 — the gadget’s total retail price.

At Goodcover, we pay the replacement cost for claims on personal property. That means you could receive the total retail cost minus the deductible when we approve your claim.

Other Advantages of Electronics Insurance With a Goodcover Renters Insurance Policy

Goodcover lets you choose from zero-deductible and premium insurance coverage plans.

Goodcover renters insurance coverage protects your wearable gadgets no matter where they are.

You’re covered whether your device gets stolen inside your condo or while backpacking in Barcelona.

But note that the deductible comes from your claim payment. So, if your deductible is higher than the value of your wearable gadget, then there’s no point in filing a claim.

Let's say you buy a $300 Oura Smart Ring, and your deductible is $500. In that case, it's not worth filing a renters insurance claim.

But filing a claim could be helpful if the same gadget is worth over $600.

Also, depending on your renters insurance policy, the claims for your wearable electronic device will be limited by:

- Per-item limits: Maximum payment per item

- Per-claim limits: Maximum payment per claim

- Category limits: Maximum payment per category

Should You Get Additional Coverage for Your Wearable Tech and Other Electronic Devices?

A standard renters insurance policy won’t cover your wearable gadget when it suffers accidental damage like pouring your morning cup of coffee all over your laptop.

But you can get additional coverage to protect your devices in the case of accidental damage by upgrading to our SUPERGOOD coverage.

SUPERGOOD coverage includes higher coverage limits, coverage for accidental damage, and zero deductible. It should be noted, however, that SUPERGOOD offers a maximum payout of $5,000 per item. So, if you want to protect individual items valued over $5,000, you may want to explore additional coverage options.

Categories eligible for SUPERGOOD upgrades include:

- Computers and other electronics

- Jewelry and watches

- Collectibles (stamps, comics, etc.)

- Cameras (excludes drones with cameras)

- Musical and sports equipment

- Bicycles

Just make sure to check your renters insurance policy claim limits on your belongings to decide which categories you may want to upgrade.

For instance, let's say you own a $1,600 TAG Heuer Connected smartwatch, and your standard renters insurance policy's claim limit is $1,500. In that case, it might not be worth getting additional coverage for your smartwatch.

But say you own a $4,000 Montblanc Timewalker E-Strap. In this case, additional coverage on the jewelry and watches category could be worth it.

You just need proof of ownership to file a claim with your insurance company. You could submit a physical or digital receipt or a credit card statement. In the case of a gifted item, you can submit a gift receipt.

Final Thoughts: A Complete Guide to Insurance for Electronics With Goodcover

Now that you know how insurance for electronic devices works under your renters insurance policy, you don’t need to fuss with extended warranties.

If your electronic device is under $1,500, your standard policy might already cover it. You can buy additional coverage for the categories that include your more expensive gadgets, which is often more affordable than an extended warranty.

Goodcover offers you better insurance coverage at half the price of legacy providers. Goodcover's renters insurance policy might automatically cover your jewelry, laptops, and wearable gadgets against theft, vandalism, and many natural disasters.

Most insurance providers provide the actual value. But we offer you the replacement cost for your damaged items.

Compare your current electronics insurance policy with Goodcover and see which gives you the better value.

Then, get a quote from Goodcover for the most affordable insurance coverage for your smart electronic devices and the peace of mind you deserve.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 1 Jul 2025 • 14 min read

Renter's Insurance Boston: A Comprehensive Guide

Dan Di Spaltro • 27 Jun 2025 • 20 min read

Renters Insurance in Rhode Island: Costs & Coverage

Dan Di Spaltro • 26 Jun 2025 • 12 min read

Nashville Renters Insurance: A Complete Guide

Dan Di Spaltro • 25 Jun 2025 • 18 min read

Iowa Renters Insurance: Cost & Coverage Explained

Dan Di Spaltro • 24 Jun 2025 • 20 min read