Extended Coverage: Increasing Coverage Limits on Valuables in Renters Insurance

6 Jul 2022 • 5 min read

Renters insurance covers your personal property against specific risks (called “perils”), such as a windstorm, theft, or fire.

But there’s a limit on how much compensation you can receive for different items. If someone takes your valuables, your personal property limits determine how much money you’ll actually get back – so they’re pretty important. And if something expensive like your DSLR camera gets damaged instead of stolen, you might not receive payment at all. So, you’ll want extra protection for these scenarios.

Enter extended coverage, or as we call it — our SUPERGOOD plan. With protection for your high-value items beyond your personal property coverage limit, you’ll enjoy peace of mind if the unthinkable happens.

Read on to learn more:

- Extended Coverage Policy

- Renters Insurance — Why You Need Extended Coverage

- What Items Can You Schedule?

- 3 Documents You Can Use for Extended Coverage Claims

- Final Thoughts: Extended Coverage — Increase Renters Insurance Coverage Limits

Extended Coverage Policy

Extended coverage broadens the scope of your insurance policy’s coverage. It supplements your standard policy and increases the coverage for your valuables.

Renters Insurance — Why You Need Extended Coverage

Goodcover renters insurance policy offers personal property coverage up to $100,000, but it’s important to note that this coverage doesn’t necessarily mean you’ll get a $100,000 payout if you suffer a loss. The policy has limits based on category, called sublimits.

For instance, if you lose $100,000 worth of jewelry from theft, you may only receive reimbursement for $1,000 worth of jewelry because it has a sublimit. So, if you’ve got expensive jewelry, premium cameras, or premium musical instruments, we recommend additional protection to ensure you can replace your items in case of loss.

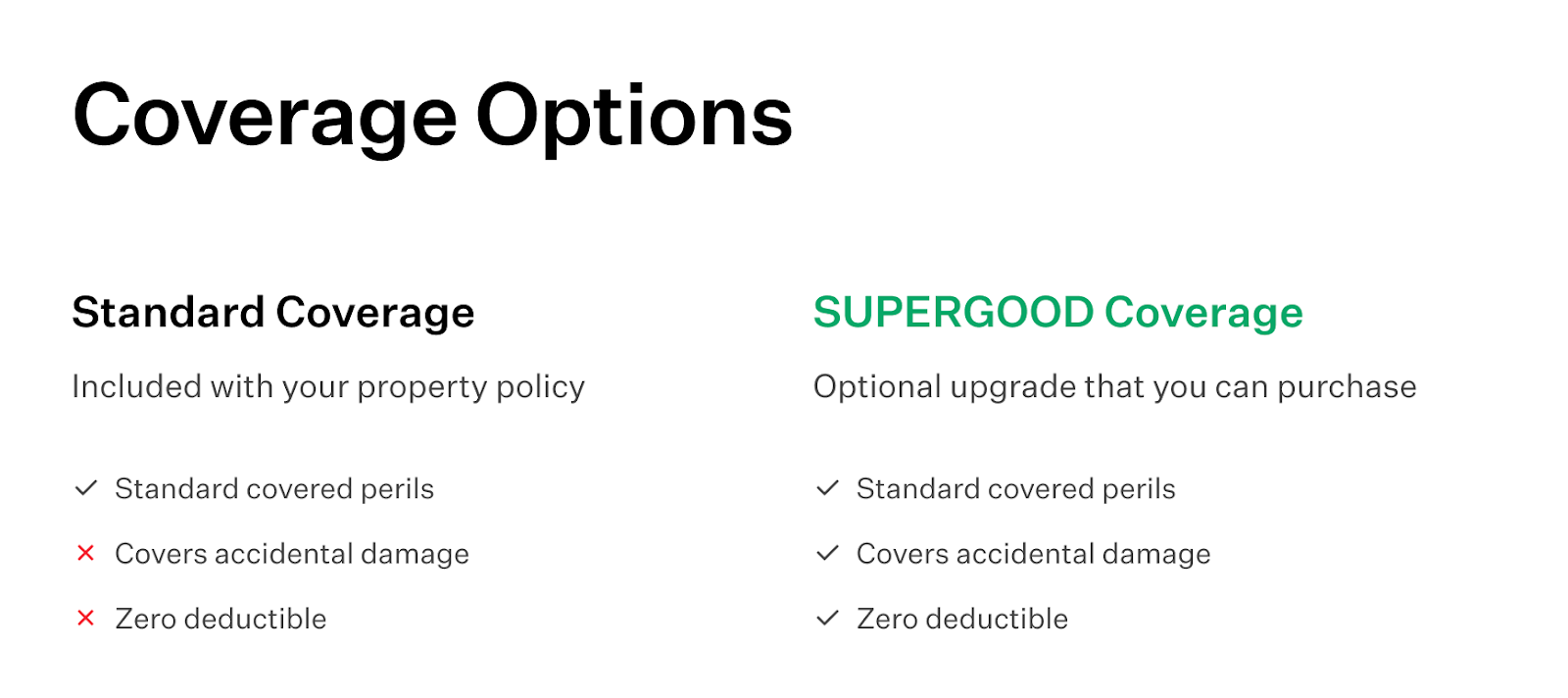

Consider insuring high-value items with our SUPERGOOD plan, which lets you purchase extended coverage for certain categories of items (like jewelry, watches, cameras, and musical instruments).Extended insurance coverage benefits you in two ways:

1. Deductible-Free Coverage for High-Value Items

If you extend the coverage limit with our SUPERGOOD plan, you’ll pay no deductible on these items. This means you’ll be able to get your item repaired or replaced without spending anything beyond your monthly premium – coming in clutch if you need to replace something like your camera lens because you accidentally cracked it.

You can get this additional coverage for a low price — especially if you choose Goodcover. Goodcover offers its Members extended coverage on certain classes of items for just a few dollars more per month.

2. Reliable Protection Against Accidental Damage

On top of letting you extend your coverage limits for certain classes of items, our SUPERGOOD plan also covers exclusions for accidental damage, like that cracked camera lens we just mentioned.

Generally, renters insurance policies without extended insurance coverage don’t cover items damaged by accident, but SUPERGOOD provides you with extra protection for your valuables.

For instance, upgrading to Goodcover’s SUPERGOOD plan gives you a zero-deductible option, so you get reimbursed at replacement cost. The plan also covers accidental damage, which means if you accidentally step on your camera and damage it, it’s covered.

What Categories Are Eligible for Increased Coverage?

A renters insurance policy usually includes coverage for the following under your personal property limit:

- Musical instruments

- Jewelry and watches

- Cameras

If you have more expensive items within one or more of those groups, you can purchase SUPERGOOD coverage for those categories with Goodcover. SUPERGOOD coverage has no deductible and covers your items in case you accidentally damage them in addition to standard perils.

To determine which categories you may want higher coverage for, check your coverage and policy limits. Certain categories of items have sublimits – the highest amount of money your insurer will pay you — for certain types of losses.

For example, say you own a watch worth $1,100, and your standard renters insurance policy has a category limit for watches of $1,000 — it might not be worth purchasing additional coverage. However, if you have $5,000 worth of jewelry and your standard policy has a limit of $1,000 on jewelry, extended coverage would make a lot of sense.

Extended coverage only applies to items that fall into the specific category that you upgraded, not any related gear. For instance, if you have increased coverage for musical instruments, the headphones and recording software you use with them aren’t covered. They’ll still be covered under your standard policy and subject to your normal deductible, but aren’t eligible for SUPERGOOD extended coverage.

Just note that while we offer extended coverage for certain categories, Goodcover has coverage limits in each category — jewelry and wearables ($20,000), cameras ($1,000), and musical instruments ($3,000). So, say you have a personal property coverage limit of $20,000 and you add $3,000 worth of SUPERGOOD for musical instruments for a few dollars more per month. If your instruments are stolen, SUPERGOOD will pay you up to $3,000 deductible-free once your claim is approved. If there’s still more to cover, you’ll need to dip into your standard insurance coverage – where deductibles and sublimits apply.

3 Documents You Can Use for Extended Coverage Claims

Certain documents are helpful if you need to file a claim with your insurance company for extended coverage.

Three types of documents you need for your claim to be eligible include:

- Proof of possession: This can be pictures of the scheduled item before and after it was damaged. It’s always good practice to maintain a home inventory.

- Proof of ownership: You can prove ownership with a receipt of the scheduled item.

- Proof of value: You can use the receipt to prove an item’s value in most cases. In some cases, you may need an appraisal – for example, proving the value of your expensive jewelry.

Final Thoughts: Extended Coverage — Increase Renters Insurance Coverage Limits

A renters policy protects your assets against covered perils, but the coverage for more expensive items may be limited. Consider getting extended coverage if you possess an expensive musical instrument, high-value jewelry or watches, or a nice camera.

Extended coverage for specific categories offers more protection than the standard limits.

With Goodcover’s SUPERGOOD plan, you also get zero-deductible coverage for the standard perils and accidental damage. Compare your current policy with Goodcover and see how you can get a bigger bang for your buck.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 15 Aug 2024 • 4 min read

Does Renters Insurance Cover Theft?

Team Goodcover • 1 Aug 2024 • 4 min read

Liability Coverage Explained: What Every Renter Needs to Know

Team Goodcover • 26 Jul 2024 • 6 min read

Colorado Renters Insurance: What You Need to Know

Team Goodcover • 6 Jul 2024 • 6 min read