The Goodcover Starter Guide to Renters Insurance in Ohio

5 Jan 2024 • 6 min read

If you’re reading this guide, you’re probably considering renting a place in Ohio. Or, perhaps you’ve felt the sting of being uninsured before and are now seeking coverage to protect yourself in the future.

As a renter, you’re joining an increasing number of Ohioans who are opting to rent over homeownership due to the tightening housing market and rising property prices. Renting in Ohio is particularly appealing, with residents enjoying 38% lower rent than the national average. The Buckeye State is an excellent place for renters.

Ohio’s appeal isn’t limited to affordability, though. Large cities like Cleveland, Columbus, and Cincinnati offer many types of experiences for a variety of people, including outdoor adventurers, sports enthusiasts, and fans of history.

Whether you’re looking to rent in Ohio long-term or bide your time until more houses hit the MLS, you have plenty of options for housing. But regardless of why you rent, the importance of renters insurance doesn’t change.

Renters insurance is essential to protect your personal property and meet lease requirements. Keep reading to learn all you need to know about renters insurance in Ohio, including how much it usually costs, what it covers, and where to find extra resources.

Here’s what this guide will cover:

- Is Renters Insurance Required in Ohio?

- How Much Is Renters Insurance in Ohio?

- What Does Renters Insurance Cover in Ohio?

- What’s Not Covered by Renters Insurance in Ohio?

- Resources for Ohio Tenants

Is Renters Insurance Required in Ohio?

The state of Ohio does not require renters insurance. However, landlords often require that you obtain renters insurance with a minimum coverage amount. Minimum coverage amounts are the limits on your renters insurance policy's different types of coverage.

For instance, a landlord might require that you have at least $100,000 in personal liability coverage. In that case, to meet lease requirements, you’ll have to provide proof that you have a renters insurance policy that meets those minimum coverage amounts before you can get the keys.

Whether it’s required by the landlord or not, getting renters insurance in Ohio is a good idea for tenants. Your landlord’s insurance only covers the building that your apartment is in. It doesn't cover your belongings, and it doesn’t provide you with personal liability protection — in other words, you’ll be financially responsible for property damage or loss that occurs.

Purchasing a renters insurance policy protects your personal items and stipulates that an insurance company pay for the costly expenses resulting from an accident in your home. Of course, there are caveats to that, which this guide will explain.

Your landlord may also ask to be named an additional interest on your policy. This simply means they’re entitled to receive notifications about your insurance policy, such as whether it’s active and how much coverage you have. However, if they ask to be second named insured, you’ll want to push back – named insureds can do everything you can do on your policy except cancel your policy. To learn more about the difference, read our blog post about the difference between additional interest and named insured.

How Much Is Renters Insurance in Ohio?

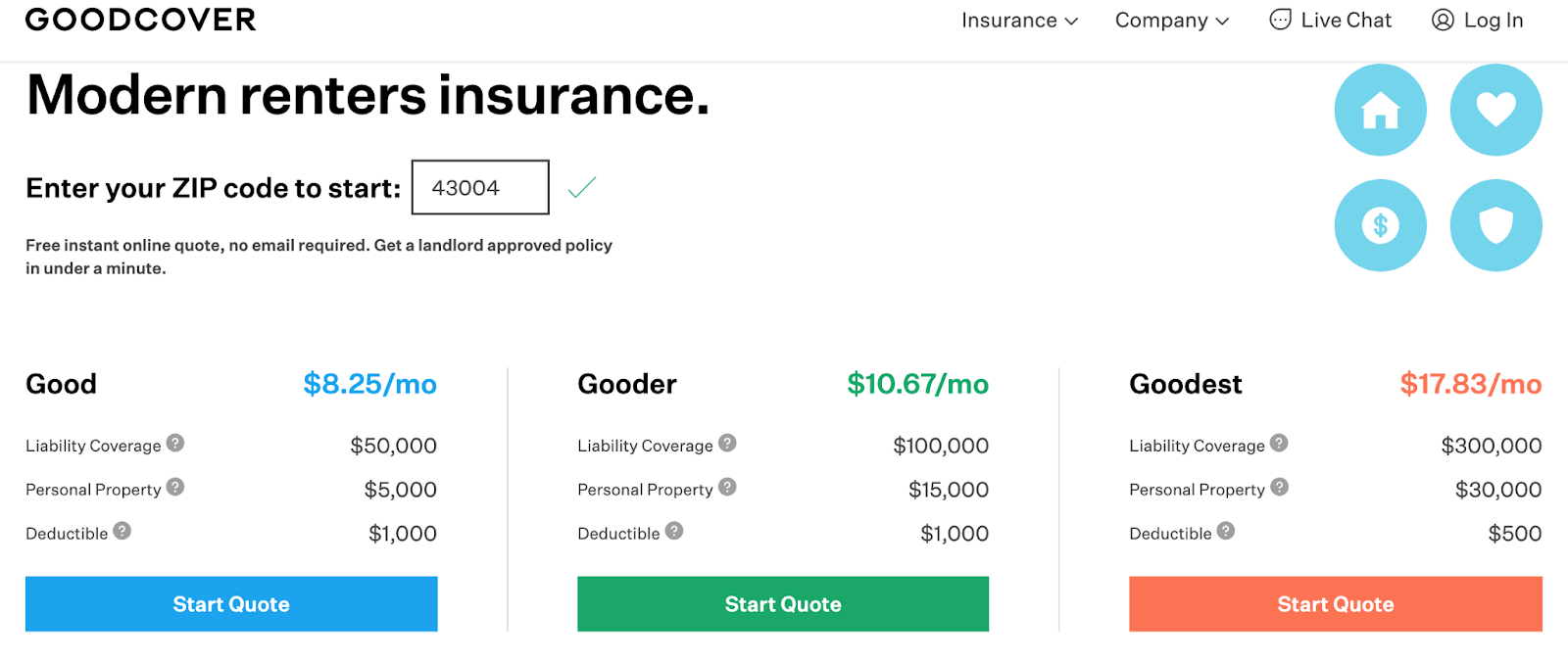

Renters insurance in Ohio costs an average of $10 per month ($124 annually). This varies based on the insurance provider you choose, the city you live in, and whether you add extended coverage for high-value items. Renters insurance rates, deductibles, and coverage limits also vary depending on the details of the plan you set up.

The best way to find out what you’ll pay for renters insurance is to get a free quote. It’s easy to do online — with Goodcover, you can get a quote faster than you can listen to your favorite song and bind your policy from the comfiest spot on your couch. Our Ohio renters' insurance plans start at $8.25 per month ($99 annually) to protect your home and personal belongings.

With Goodcover, you also get flexible coverage options to tailor your policy to your needs. You can increase coverage limits for maximum protection or lower your amount of coverage to reduce your monthly premium.

The best part is you can build the perfect plan from the comfort of your home. You won’t need to go through an insurance agent, make any phone calls, or sign any paperwork.

Now, let’s discuss the different scenarios and belongings you can cover with renters insurance.

What Does Renters Insurance Cover in Ohio?

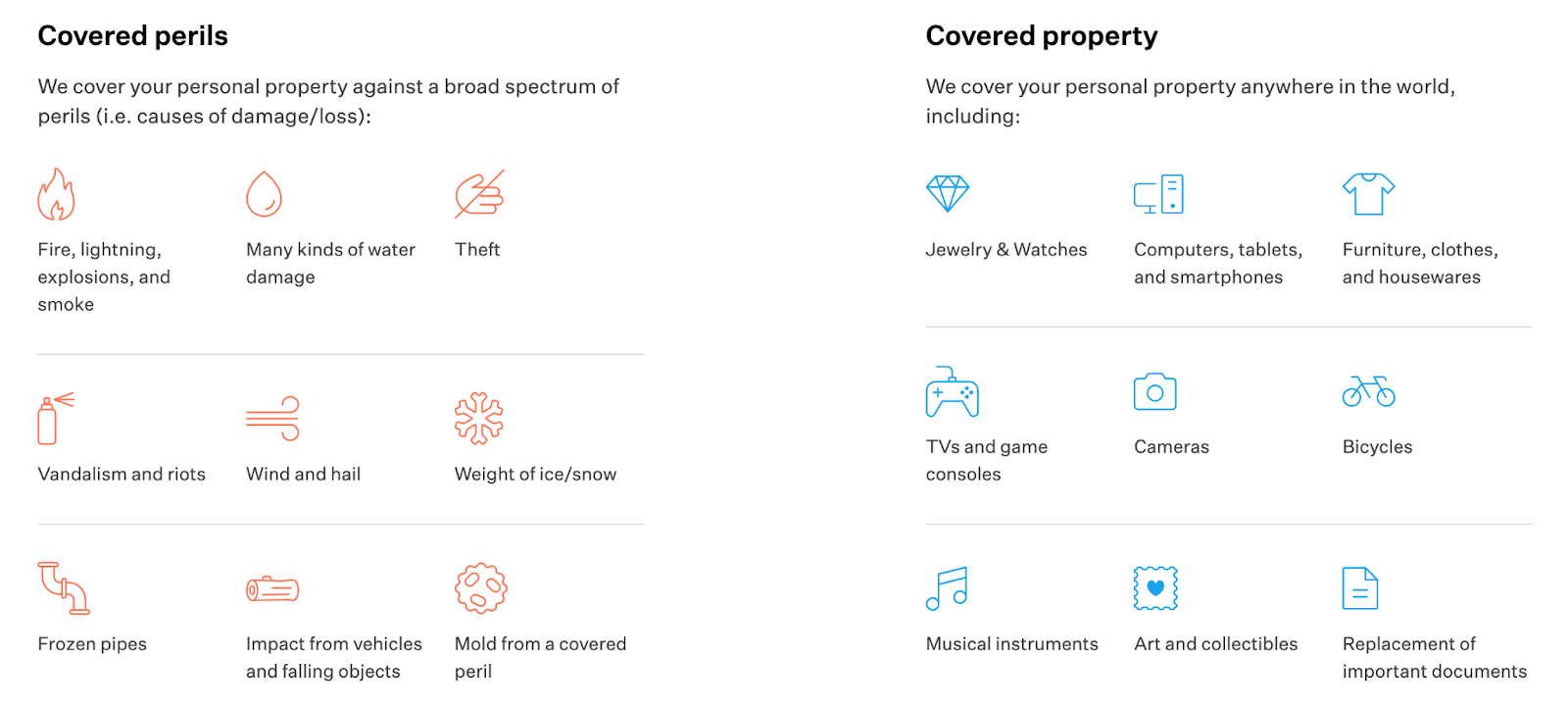

Your Ohio renters insurance will cover your personal property in case of loss or damage due to covered events like vandalism and fire. In addition to personal property coverage, your renters insurance policy will offer liability protection and loss of use. That’s insurance jargon, but we promise you’ll understand all three by the end of this section.

Personal Property Coverage

Personal property is the primary subject of your renters insurance policy. It covers the cost of your items if they are damaged or destroyed in situations like a fire, explosion, hail, riots, and theft. This type of coverage can apply to belongings like important documents, art, clothes, and bikes, for example.

If you live in Ohio, there’s a one in 54 chance of becoming a victim of a property crime. With the average cost of renters insurance in Ohio only running $124 annually, it really doesn’t cost much to have peace of mind.

And if you have expensive possessions — like jewelry, musical instruments, and cameras — you can purchase extended coverage that protects those assets.

In addition to knowing your coverage limit, you want to see how each insurer calculates the amount of money they’ll reimburse you for ruined or stolen items: replacement cost value or actual cash value.

Goodcover uses replacement cost value (RCV) to determine how much to pay you for a covered loss; in other words, you get reimbursed for the full amount needed to replace your ruined or stolen item with a new one.

In contrast, some other insurers only allow an actual cash value (ACV) minus depreciation; in other words, they detract some of the reimbursement based on how used or old your possessions were. Meanwhile, you’ll probably pay more for a brand-new item to replace it.

Goodcover’s RCV calculation could mean you avoid dipping into your savings even after filing a renters insurance claim.

Temporary Housing (Loss of Use)

Temporary housing coverage, also referred to as loss of use or Coverage D, is included in the personal property section of your renters insurance. This part of your policy covers additional expenses incurred if you need to vacate your home and find another place to live because of a covered incident.

For instance, say your neighbor leaves a space heater running during a winter storm, and a fire breaks out that damages your home. You have to stay in a hotel during repairs. Temporary housing coverage helps you pay for your additional living expenses, such as the additional cost of your hotel room and additional gas than you’d normally use for your commute to work.

Liability Protection

Personal liability coverage grants you financial protection if you’re liable for an incident that occurred in your home, such as an acquaintance coming over and having an allergic reaction to that great new dip you picked up at West Side Market. With Goodcover, liability protection will help pay for related legal fees and medical payments.

What’s Not Covered by Renters Insurance in Ohio?

Renters' insurance policies cover a lot, but they don't cover every incident. That’s why it’s important to understand your policy’s exclusions before you commit.

For example, most renters insurance companies don’t cover:

- Certain natural disasters: Wildfires, floods, and earthquakes are usually covered by supplemental insurance, which is a different thing. Goodcover can help you add supplemental earthquake insurance through our partner, Palomar.

- Catastrophic events: Renters insurance doesn’t cover damage and loss caused by extreme events such as nuclear hazards and government seizures.

- Vehicles: Goodcover can protect the belongings within your vehicle, but the vehicle itself requires auto insurance. Note that renters insurance can cover some classes of e-bikes as well as manual bicycles.

- Intentional damage: Insurance doesn’t cover deliberate damage you inflict on your property.

- Accidental damage: By default, renters insurance doesn’t cover accidental damage like dropping your designer sunglasses off the balcony at Old Arcade. However, you can get renters insurance coverage for accidental damage by using Goodcover’s SUPERGOOD plan.

Resources for Tenants in Ohio

Get the most out of your rental experience by understanding the rules and regulations on renting in Ohio. Here are some resources to assist you while renting:

- Ohio's tenant rights, laws, and protections.

- Federal fair housing laws applicable to Ohio.

- Ohio renter’s kit with placement and payment programs.

With lower-than-average rent prices, Ohio is a great place where people can enjoy big cities and access 75 state parks. Wherever you settle in the state, getting Ohio renters insurance is an affordable and effective way to protect your home and property.

With Goodcover, you can get a free renters insurance quote from the comfort of your couch (in less time than it takes to jam out to your favorite song) because no agents or paperwork are required. See for yourself and get a quote today.

Note: This post is for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 18 Jul 2025 • 21 min read

Most Affordable Renters Insurance: A Complete Guide

Dan Di Spaltro • 17 Jul 2025 • 18 min read

Affordable Renters Insurance in Florida: Top Picks for Savings

Dan Di Spaltro • 16 Jul 2025 • 22 min read

Your Guide to Affordable Renters Insurance

Dan Di Spaltro • 15 Jul 2025 • 16 min read

Does Renters Insurance Cover Theft? A Simple Guide

Dan Di Spaltro • 14 Jul 2025 • 15 min read