Goodcover’s Complete Guide to Renters Insurance in Houston

11 Mar 2024 • 6 min read

Houston is the largest city in Texas, with over 2.3 million residents, and a staggering 58% of homes are for rent.

According to the Houston Association of Realtors, listings for single-family homes for rent increased 16% between June 2022 and June 2023. And leases of townhouses and condominiums rose 15.3% in the same period, showing both an increase in supply and a strong demand for homes to rent.

If you’re among the many new renters in the city, you’re likely in the market for a new renters insurance policy. You may have questions about what’s required, what’s covered, and what your choices are. This guide to renters insurance in Houston will answer all of those questions and more.

Here’s what we’ll go over:

- Do I Need Renters Insurance in Texas?

- How Much Is Renters Insurance in Houston?

- What Does Renters Insurance Cover in Texas?

- Resources for Houston Tenants

Do I Need Renters Insurance in Texas?

Texas is one of several states that doesn’t legally require renters insurance. That said, landlords in the Lone Star State can require renters insurance as part of the lease agreement. It’ll be clearly outlined in the lease agreement — and your landlord will probably mention it to you — if it’s required.

There’s a good reason that so many landlords want tenants to have renters coverage, too. Renters insurance in Texas protects you from property damage related to crime, like vandalism or theft. So, you’ll definitely see this requirement pop up in larger cities like Dallas, Austin, and San Antonio.

And crime is something all Houstonians should consider, too. While violent crime in the city decreased 12% in the first quarter of 2023 compared to a year ago, burglaries increased 2%. With a renters policy, you’re covered in the event of a burglary.

Renters insurance in Houston, TX, may also help with both the replacement cost of your items and damage resulting from the effects of natural disasters, like hailstorms, tornadoes, or windstorms.

Finally, renters insurance doesn’t just protect your personal belongings. It also includes personal liability coverage. This part of your policy kicks in if you’re found responsible in a lawsuit or for a guest’s injuries at your home.

How Much Is Renters Insurance in Houston?

The average cost of renters insurance in Houston can vary a bit. Factors like the type of building you live in, where it is, and how large your unit is can all impact the price of your policy. The cost also will go up if you have any valuables you want additional coverage for.

Each insurance provider you contact will offer different amounts of coverage, and some might have a higher deductible than others.

Basically, you’ll need to get a renters insurance quote to know exactly what you can expect to pay. Luckily, getting a quote for renters insurance is easier than ever. In fact, Goodcover can get you one faster than you can listen to your favorite song

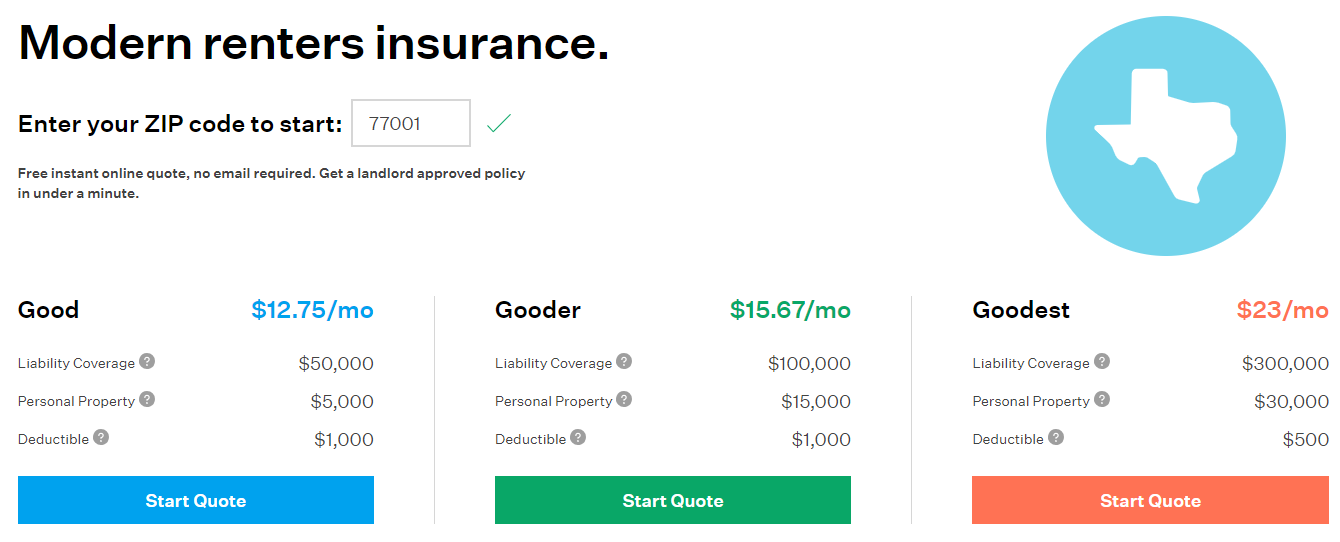

With Goodcover, rates for Houston residents start around $12.75 per month or roughly $150 per year. That means you could have secure renters insurance for less than 50 cents a day.

Your Goodcover policy will cover things like your personal belongings and medical expenses for people injured on your property if you’re found liable. It will even help with some of the costs of temporary housing if you can’t use your home for a while.

What Does Renters Insurance Cover in Texas?

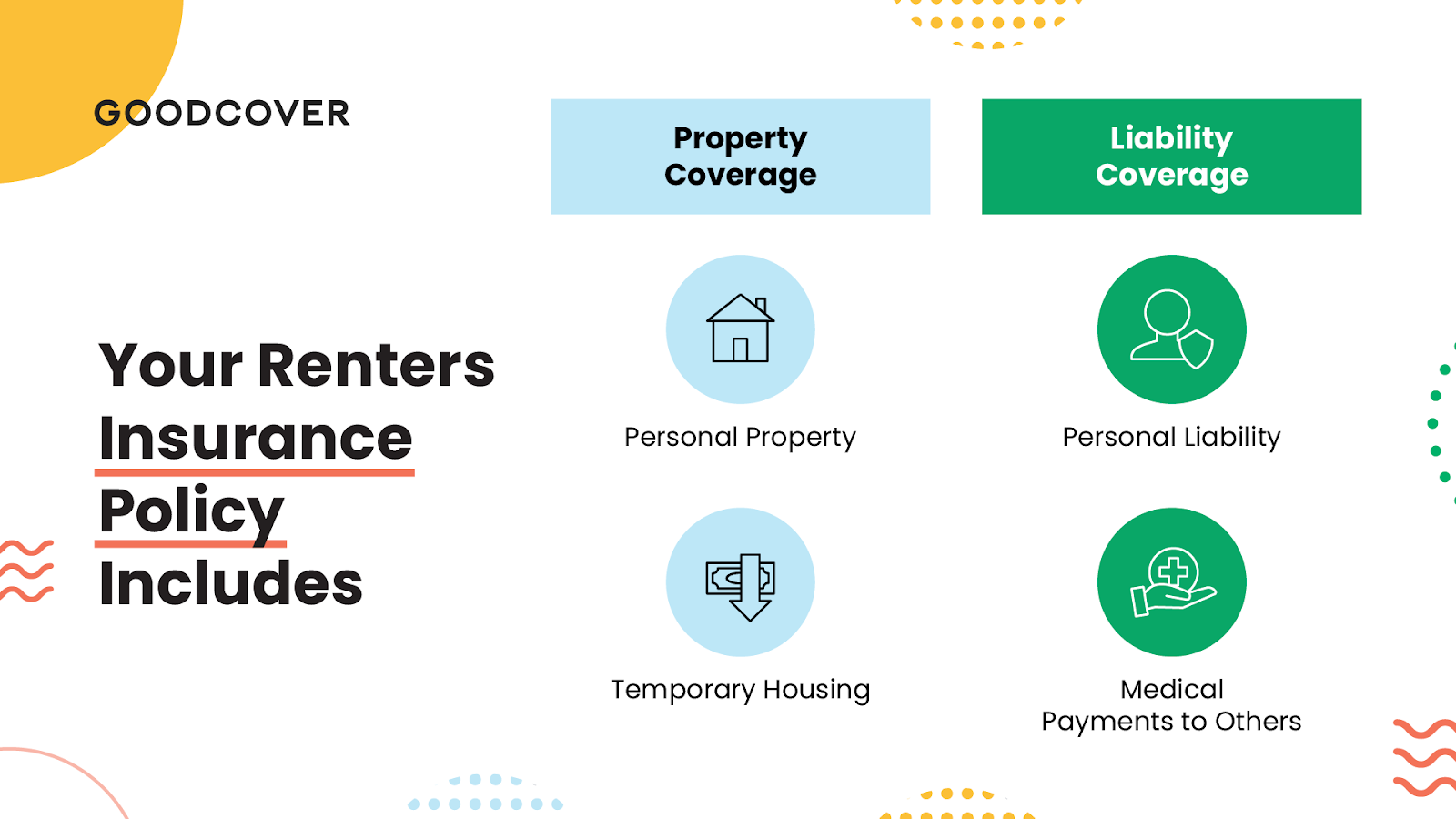

You’ll find that Texas renters insurance covers a few different ways to help you out in an emergency. Your insurance company may have these categorized differently, but most policies include two main categories: liability and personal property coverage.

Liability Protection

This part of your policy helps cover damage you’re found responsible (aka liable) for. For instance, if a friend slips on your wet floor and needs to go to the hospital.

This category is usually further divided into your personal liability and medical payments to others you may be required to cover.

That means you’ll have a set amount that helps cover medical expenses you’re liable for, as well as another amount for things like accidental damage to your apartment. Say your roommate is on your policy, and they accidentally damage the front door while moving some furniture. Your liability protection could cover the cost of this damage after you hit your deductible.

A typical Goodcover policy offers between $50,000 and $300,000 in liability coverage. Remember, this also covers any legal fees you might accrue over the course of an insurance claim.

Personal Property Protection

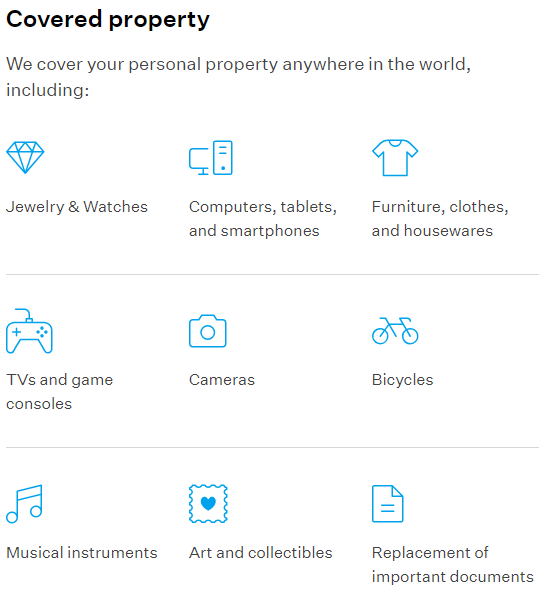

The other main segment of your renter's insurance policy covers loss or damage to your personal property (in other words, your stuff). For example, if a burst pipe causes water damage to your laptop or if someone steals your bicycle from your garage, your personal property coverage will help repair or replace your items.

You’ll have several coverage options here, including the ability to add additional coverage for collectibles or other valuable items. If you do have any extra-special items, it’s probably worth looking into more coverage for them.

There’s also a section called temporary housing coverage. It’s sometimes called Coverage D or loss of use. This helps cover any money you might have to spend when you can’t use your home temporarily, including for temporary housing.

For example, maybe there’s a small electrical fire, and you need to stay in a hotel for a few days while your landlord takes care of any smoke damage. Your insurance can help cover those additional living expenses.

Natural Disasters

Your policy may also cover many of the natural disasters that affect the Houston area. So, the next time a strong windstorm rolls in, you can rest assured that the damage to your unit may be covered by your landlord’s insurance or yours.

In addition to wind damage, renters insurance may cover hail, lightning, and some of the damage caused by hurricanes.

What Does Renters Insurance Not Cover?

It’s important to remember that renters insurance doesn’t cover everything. Nearly all Houston renters insurance policies have certain exclusions.

A big one is flooding. And since 1 in 7 properties in Houston has a “substantial” flooding risk, you might also need to carry flood insurance. Unfortunately, Goodcover is unable to offer this type of coverage. However, you can get a flood policy through the National Flood Insurance Program.

You’ll also need separate auto insurance if you drive, as most rental policies won’t protect your car, either. That includes any damage your car may do to the property or if your vehicle is vandalized at your home.

Your policy likely will exclude most damage caused by a pet, too. Of course, if you’re worried about your furry friend causing damage, there is pet insurance, as well.

If you have any questions about what your policy covers, it’s better to ask before major event happens.

Resources for Houston Tenants

We know knowledge is power, and staying informed is how you can find the best renters insurance in Houston for you. That’s why we’ve compiled a list of resources to help you find out even more about renting a home in Houston.

These resources cover everything from your rights as a tenant to locating affordable housing in the city:

- Tenants’ Rights Handbook

- City of Houston Rental Information

- Houston Apartment Association Renters Services

- Harris County, Texas, Housing Search

- Houston Housing Authority

While trying to understand how renters insurance in Houston, TX, works can be a bit challenging, at Goodcover, we think insurance should be as straightforward as possible.

When you understand what a policy covers and how much it costs, you can pick the coverage that makes sense for you.

Contact Goodcover today to get transparent, landlord-approved coverage.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 26 Jul 2024 • 6 min read

Colorado Renters Insurance: What You Need to Know

Team Goodcover • 19 Jul 2024 • 6 min read

Goodcover’s Guide to Ohio Rent Increase Laws: Know Your Rights as a Renter

Team Goodcover • 6 Jul 2024 • 6 min read

6 Renters Insurance Mistakes (and How to Protect Yourself)

Team Goodcover • 26 Jun 2024 • 8 min read

How to Get Renters Insurance

Team Goodcover • 7 Jun 2024 • 3 min read