Is Camera Insurance Worth It? What You Need To Know

19 Jan 2024 • 6 min read

Ever seen a photographer slip and fall? In that split second, their instinct often kicks in like a reflex. Suddenly, their arm lifts to protect their camera from harsh impact on the ground. It’s an almost comical sight, but it speaks to the love photographers have for their gear. After all, photography equipment isn’t cheap whether you’re a Canon, Nikon, Sony, Fujifilm, Panasonic, or Pentax fan.

A single stolen or damaged camera could cost thousands of dollars to replace and derail your passion. But is standalone camera insurance worth the extra cost and effort to obtain? Or can you cover your camera gear through your renters insurance?

What types of camera gear insurance are available? How much does insurance cost? Does it cover your camera outside your home? Is water or fall damage excluded? Are group and business policies an option if photography is part of your livelihood?

In almost every case, having coverage for your camera can save you money and heartache.

Keep reading as we dive into what camera insurance covers, key insurance policy options, and how to determine what's right for your needs.

Here’s what we’ll cover:

- Camera Insurance Basics: Why It Matters

- Does Renters Insurance Cover Cameras and Photography Equipment?

- Is Camera Insurance Worth It?

- How Much Does Camera Insurance Usually Cost?

- What Should I Ask When Shopping for Camera Insurance?

- Final Thoughts: Is Camera Insurance Worth It? What You Need To Know

Camera Insurance Basics: Why It Matters

The necessity of camera equipment insurance becomes apparent when you consider the hefty price of a photography hobby. Cameras and lenses, regardless of brand – be it Canon, Nikon, Sony, or Sigma for lenses –are significant investments.

For instance, the Canon EOS 5D Mark IV DSLR retails for around $2,700 for just the camera body, excluding additional expenses for lenses, memory cards, bags, and flashes.

Everyone hopes their photography equipment is never stolen, dropped, or damaged. But sometimes it happens, often when you least expect it, turning your hobby into a financial burden overnight

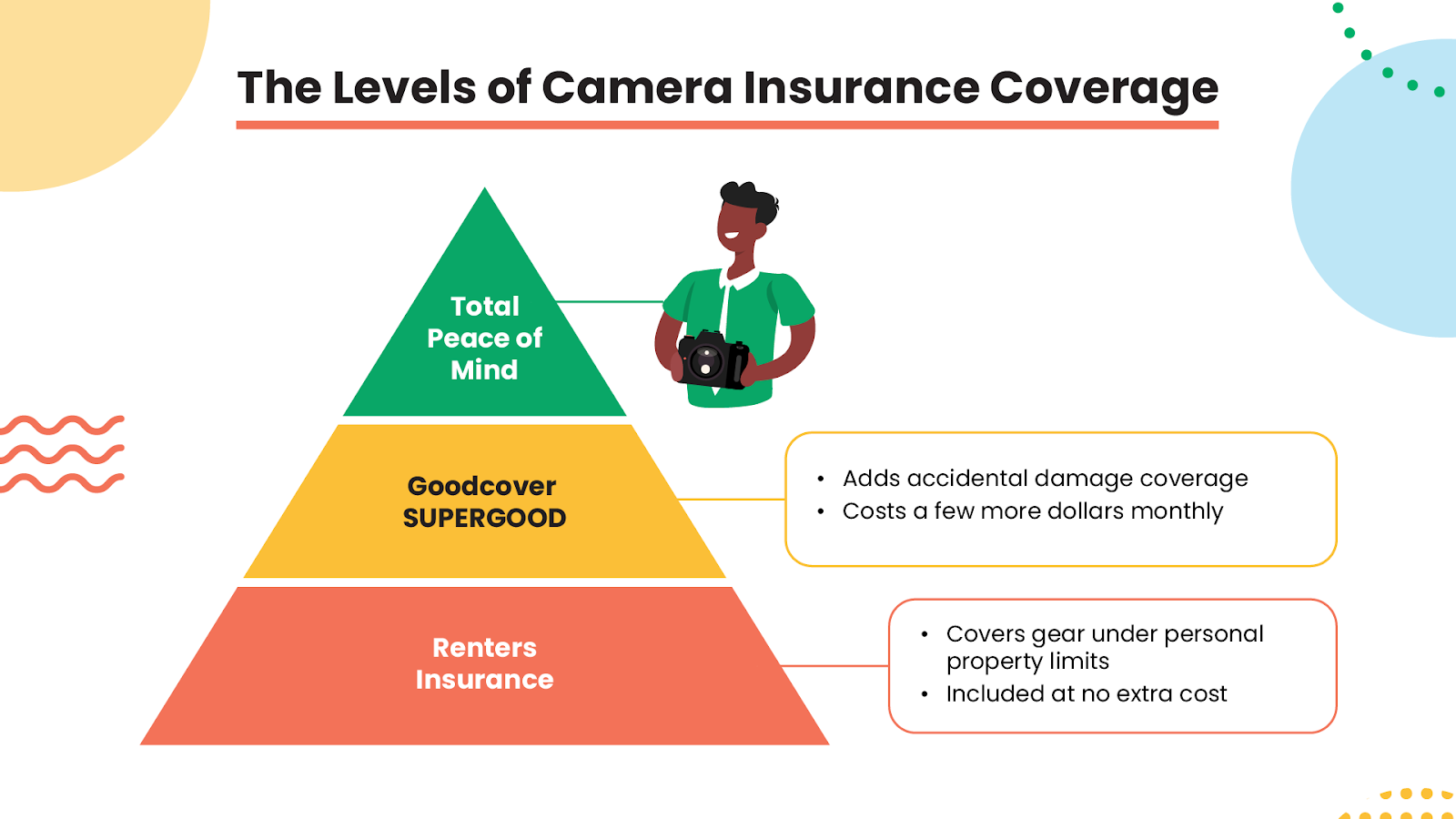

Fortunately, camera equipment insurance offers a solution. Whether it’s a standalone policy or coverage through your renters insurance, it provides a financial safety net.

Your renters insurance considers your camera accessories like the bag and tripod part of your personal property. If you need extra coverage for your camera itself, including coverage for accidental damage, it’ll only cost a few more bucks a month with Goodcover’s extended coverage option.

Does Renters Insurance Cover Cameras and Photography Equipment?

When planning how much insurance you need, knowing what is and isn’t covered for your photo gear is important.

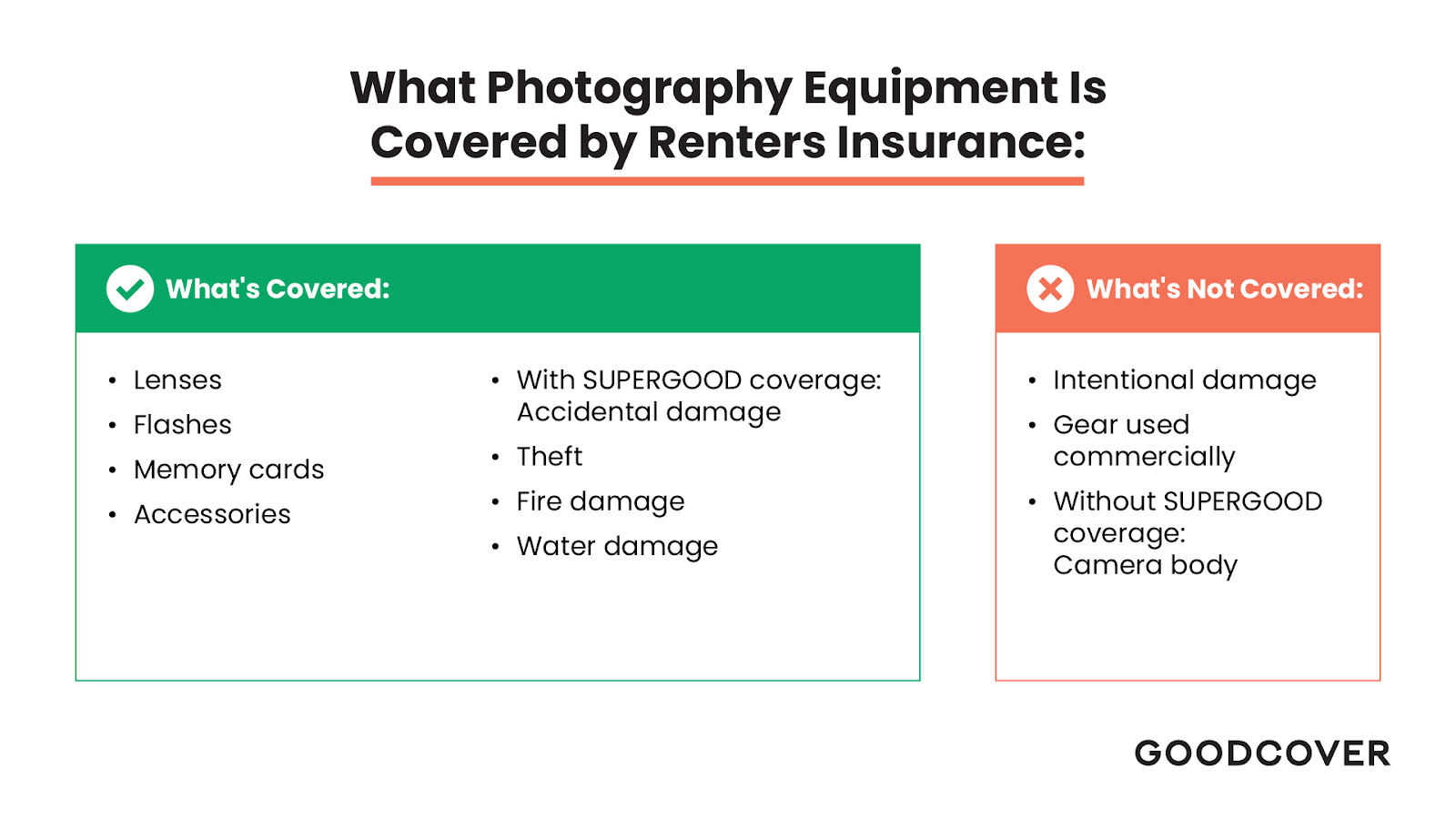

What Renters Insurance Covers

Renters insurance includes valuable coverage for your photography gear against common hazards like theft or fire under the personal property damage section of policies.

Within your contents coverage limits, items like camera bodies, lenses, flashes, lighting equipment, backdrops, memory cards, bags, and other photography accessories qualify as covered personal possessions. For Goodcover members, coverage extends to damage or loss from theft, fire, water leaks, and other covered perils.

However, standard plans generally limit electronics claims beyond a specified value. Goodcover offers a SUPERGOOD plan option, which includes extended coverage for specific items like jewelry, musical instruments, and cameras up to $1,000.

If your gear costs more than that, you can only be reimbursed $1,000 for the maximum claim payout. Extra accessories would fall under your normal personal property limits.

However, Goodcover offers replacement value coverage, so they won’t depreciate your gear like actual cash value insurers do. So you’ll get a full payout up to the maximum instead of being told the camera you paid $1,000 for six months ago is only worth $500 now because a new model came out.

Plus, under Goodcover’s SUPERGOOD coverage, you’ll also be covered for those pesky accidents that you can’t predict, whether at home or traveling with your camera. So you’re covered if you are shooting waterfalls and your camera takes a swim after you slip on a rock.

What Renters Insurance Doesn’t Cover

Renters insurance personal property coverage offers great protections, but there are limits to coverage. Some items not covered include:

- Accidental damage: Damage caused by dropping your gear or spilling something on it typically isn't included in standard plans. So, while fire or theft may be covered, clumsiness exclusions leave your equipment vulnerable unless you purchase extended coverage. You need to purchase SUPERGOOD coverage for accidental damage coverage on your camera.

- Intentional damage: Deliberately damaging photography equipment is never covered, so tossing the camera down the stairs isn’t a shortcut to getting a newer model.

- Commercial use: Using camera gear for any commercial purpose is excluded. This also means that your renters insurance personal liability coverage won’t kick in if the situation results from business camera use.

While renters insurance covers most of your needs, professional photographers will need to consider standalone photographer insurance for their photography business. If you use your camera for business, you’ll need to consider standalone business owner’s policies (BOPs) that bundle commercial property coverage with general liability insurance and loss of business income protections.

Is Camera Insurance Worth It?

Worrying about damaging your camera can suck all the fun out of photography. Boat rides, cycling, rough hiking trails, or even worrying about rain can leave photographers feeling like they must choose between the hobby they love and protecting their gear.

Getting extended coverage to cover your valuable equipment for a few extra bucks a month lets you enjoy your hobby without fear. For example, if you live in California and you want to add the $1,000 extended camera coverage, it’d only cost you $1.54 more per month on a standard plan.

How Much Does Camera Insurance Usually Cost?

Your Goodcover renters insurance plan automatically protects your camera equipment under the personal property coverage limits at no additional cost, and you can add extended coverage at minimal cost.

Plus, Goodcover’s SUPERGOOD coverage only costs a few dollars extra each month if you want extended coverage for accidental damage. SUPERGOOD adds extra protection for your camera if it suffers a covered peril outside of the home.

Goodcover’s standard coverage includes 10% of your personal property limit for perils that occur outside your home. But SUPERGOOD overrides that coverage, ensuring a deductible-free payout up to your coverage limit for the full amount, even if you’re not home when the loss occurs.

What Should I Ask When Shopping for Camera Insurance?

When evaluating camera insurance coverage options, look beyond the premium pricing. A plan may seem too good to be true until you look at the exclusions.

For example, a plan that only covers your camera when it’s sitting unused at home isn’t as helpful as a plan like Goodcover’s SUPERGOOD that protects you while using the equipment.

Ask these key questions before buying and compare to Goodcover's straightforward protections:

1. What damage types and losses are excluded? For example, Goodcover’s SUPERGOOD includes accidental damage and common mishaps without convoluted exemptions.

2. Does the plan use actual cash value (ACV) or replacement cost value (RCV)? Goodcover always uses replacement cost values, not depreciated sums that leave you unable to replace your equipment.

3. What varieties of photography equipment are explicitly covered? Make sure your camera insurance policy's defined "covered property" aligns with the gear you own now (or soon plan to).

4. For basic accessories like camera bags, what coverage terms apply? Some plans revert to blanket personal property rules vs. tailored camera equipment coverage.

5. When and where does coverage apply? On-location shoots deserve just as much attention as home storage. Be sure you know where your policy covers your gear.

6. What are my deductible options? Some insurance providers might require a higher deductible when filing a camera claim.

Final Thoughts: Is Camera Insurance Worth It? What You Need To Know

Securing camera equipment coverage with a reputable insurance company provides incredible peace of mind, letting your photography passion truly flourish wherever inspiration strikes.

Camera insurance as part of your renters insurance safeguards expensive gear from inevitable mishaps and enables pursuing dynamic shoots, knowing your coverage has your back.

While standard renters insurance options supply basic defense, you can add Goodcover's flexible SUPERGOOD additional coverage protections to ensure you have the right amount of coverage and reduce equipment upgrade anxiety for just a few bucks more per month.

Relax and shoot confidently, knowing Goodcover offers the coverage you need. Get a free quote today so you can get back to shooting fast.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 26 Jul 2024 • 6 min read

Colorado Renters Insurance: What You Need to Know

Team Goodcover • 19 Jul 2024 • 6 min read

Goodcover’s Guide to Ohio Rent Increase Laws: Know Your Rights as a Renter

Team Goodcover • 6 Jul 2024 • 6 min read

6 Renters Insurance Mistakes (and How to Protect Yourself)

Team Goodcover • 26 Jun 2024 • 8 min read

How to Get Renters Insurance

Team Goodcover • 7 Jun 2024 • 3 min read