Everything You Need To Know About the Renters Insurance Claim Process

24 Nov 2023 • 5 min read

Filing a renters insurance claim isn’t complicated. It’s just a tad procedural. In this guide, we walk you through the five-step renters insurance claims process so you’re always in a position to tap into your insurance protection whenever you need to.

How to File a Renters Insurance Claim

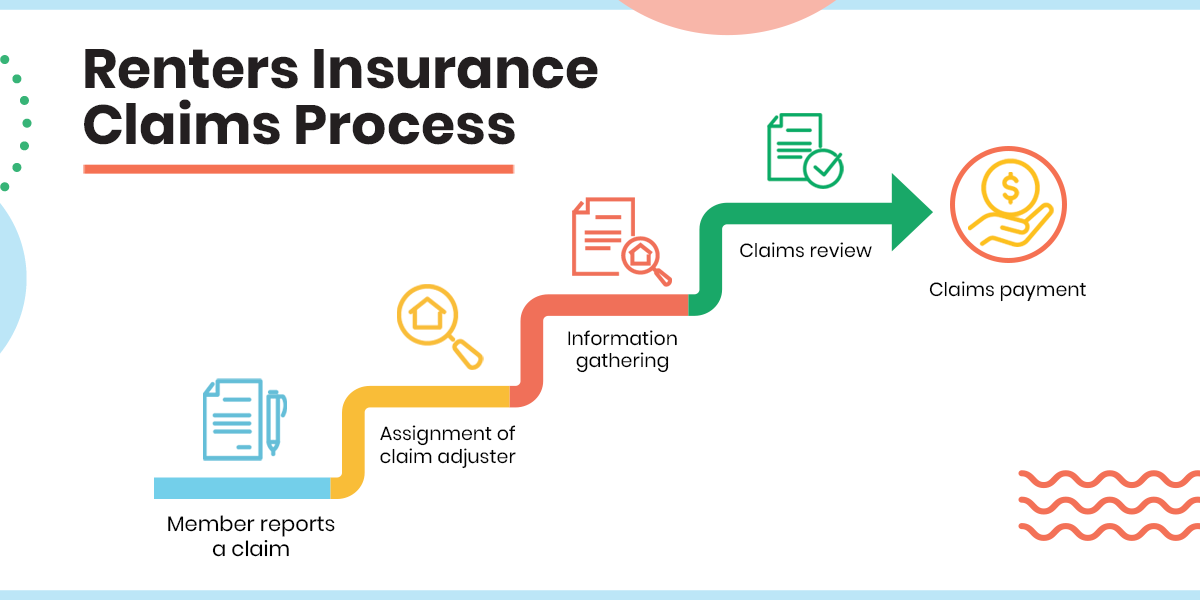

Here’s how to file a claim with Goodcover in five simple steps.

Step 1: Member Files a Claim

The first thing you should do is report the claim. We’ve teamed up with Fortegra to assist us with claims. They’re pros who help you through the insurance claims process.

So, you’ll be chatting with a friendly agent throughout your renters insurance claim. They will collect information from both you and Goodcover. We’ll provide them with a copy of your policy and any other relevant information, such as when your policy went into effect and if you’ve made any changes. That way, everyone is on the same page as we work through your claim.

To get started, you can email Member Experience at claims@goodcover.com, and we’ll redirect you to the proper claims adjuster.

You can also log into your Goodcover Member Dashboard, which redirects you straight to our claims partner.

In the insurance world, this claim report is known as the first notice of loss (FNOL). It’s the first step to tackle your claim, and it must be filed immediately. We want to get things rolling for you as quickly as possible! When you file your FNOL, you’ll be asked to provide some details, such as:

- Your name

- Contact information

- Insurance information

- Location of the loss

- Type of loss

- Date and time of loss

- Other information about what happened

Step 2: Assignment of a Claims Adjuster

Next, we will assign someone to take a close look at your claim and figure out what coverage applies to your loss, as well as how much money you should receive in compensation.

This person, called an adjuster, will carefully evaluate the extent of damage to your property. They will take into account everything you’ve shared about the incident, the police report, and any eyewitness testimonies.

Once the adjuster takes over, they’ll be your go-to person for any questions you have about the status of your claim. They’ll keep you updated on the progress of your claim, ask for necessary information from you, and share the relevant information with your insurance company. So, don’t hesitate to reach out to them if you’re curious about anything.

We may also be able to help you access your payouts earlier in case of hardship. For instance, our Members’ claims for temporary housing arrangements spiked in August 2021 in California due to the wildfires that burned over 2.5 million acres. Several of our Goodcover Members requested an advance on their loss of use coverage (which is usually a reimbursement check) to pay for the exceptionally high cost of lodging – and we approved it. We care about our Members, so if you’re ever in a situation like this, don’t hesitate to ask us if there’s anything we can do.

Step 3: Information Gathering

To keep things rolling smoothly, your adjuster will request information and documents from you to assess the cause and damage. This is super important: the quicker we can get this information from you, the faster we can settle your claim. Documents we may request include:

- inventory of the damaged property

- photos of the damage

- proof of purchase or ownership for damaged items

- proof of identity

- and other documents related to your loss

It’s important to have proof of ownership for the items included in your claim. While purchase receipts are one of the most commonly used forms of proof, there are plenty of ways you can verify ownership, so you don’t have to worry if you’ve already thrown away that receipt.

Insurance providers use proof of ownership to make sure people aren’t filing fraudulent claims and trying to get paid for items that aren’t theirs.

Documents that can support your proof of ownership include:

- Purchase receipts

- Credit card or bank statements

- Appraisals or valuations

- Photos or videos of the item in your home

- Original packaging or product documentation (such as user manuals)

- Online registration for electronics

If your loss is significant enough that you’ll have to relocate, renters insurance can help cover those costs too. In that case, you can likely claim temporary housing coverage or "loss of use," as it's known in the insurance world. You'll need receipts for ongoing living expenses if you're claiming this coverage.

Claims adjusters also verify complex claims in collaboration with a Special Investigations Unit (SIU). If the claims adjuster and SIU look into the case, you shouldn’t be concerned — it’s just part of doing due diligence.

Following these steps ensures that none of the claims are fraudulent or exaggerated. Examples of fraudulent claims include tampering with the police report and getting an insurance policy after an accident.

Step 4: Claims Review

Making progress! At this stage, your insurance adjuster will start the assessment after you’ve submitted all the necessary information. You can contact your claims adjuster for status updates on your claim. They’re there to keep you in the loop!

Once the adjuster has reviewed the information and assessed the estimated damages, exclusions, available coverage, and relevant extended blanket coverage categories, they’ll communicate all the relevant information to you.

Remember when we said it was super important to communicate promptly with us? Here’s why: if you don’t provide the requested documents or additional information in the previous step after multiple requests, the adjuster will send you a 14-day notice.

The claims adjuster will close the claim if you fail to respond to the notice with the requested documents within that 14-day time limit. Please reply promptly to requests from the claims adjuster. We don’t want to

make you start all over from scratch!

Step 5: Claims Payment

At this point, the adjuster can issue the final payment based on your policy’s terms.

When the payment is lower than the deductible or outside the scope of your renters insurance coverage, the claims adjuster will explain everything to you in writing.

You can receive funds via your preferred method — a direct deposit (ACH) or mailed check. From the time your claim is approved, it can take up to two weeks to receive this deposit.

After the Payment

If you recovered the loss, you’re probably patting yourself on the back for deciding to pay renters insurance premiums. But don’t just smile your way to the bank and call it a day. You should still ensure that you have enough insurance coverage for your future needs.

Note: This post is for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 16 Aug 2024 • 2 min read

Goodcover Weekly Recap | Week of August 11, 2024

Team Goodcover • 9 Aug 2024 • 2 min read

Goodcover Weekly Recap | Week of August 4, 2024

Team Goodcover • 13 Jun 2024 • 6 min read

Renters Insurance and Roommates: Share and Save with Goodcover

Christopher Lotz • 2 Oct 2023 • 5 min read