How Am I Covered Under My Renters Insurance Personal Liability?

23 Feb 2022 • 5 min read

Renters insurance protects more than just your personal belongings. It protects you. Besides personal property coverage, standard renters policies include temporary housing and personal liability coverage.

Having renters insurance and understanding all the ways you’re covered can end up saving you thousands of dollars if accidents happen in your apartment.

In this article, we’ll cover everything you need to know about the personal liability coverage you get with renters insurance.

Here’s what you’ll learn:

- Understanding Liability Insurance

- What Is Personal Liability Coverage for Renters Insurance?

- Situations Covered by Personal Liability Insurance

- What’s Not Covered by Personal Liability Insurance

- Choosing Your Personal Liability Coverage Limits

- Final Thoughts: What Does Personal Liability in Renters Insurance Cover?

Understanding Liability Insurance

Liability insurance is a type of coverage that gives you financial protection for claims made against you involving unintentional injury or property damage. Businesses and individuals can both purchase liability insurance.

Some people receive personal liability protection through their homeowners insurance. If you’re not a homeowner, you can still get liability coverage through a renters insurance policy.

What Is Personal Liability Coverage for Renters Insurance?

Personal liability coverage is one of three standard coverages you receive in a renters insurance policy (the other two are personal property and loss of use). Personal liability coverage helps cover your expenses if you’re found legally responsible for someone else’s injuries or property damage.

Specifically, your coverage can help pay for another person’s medical bills or the cost to repair or replace damaged property. Personal liability coverage can also pay for your legal defense, even if you’re not found liable.

Your personal liability coverage does not apply in cases of intentional injury or damage.

It’s important to know that your landlord’s insurance policy on the building does not protect you if someone is injured in your rental unit. That’s why many landlords may require that you purchase a renters insurance policy.

Situations Covered by Personal Liability Insurance

So, when can you be held legally responsible for someone else’s injury or property damage?

In general, if an accident or property damage occurs in your residence, you can be held legally responsible if you fail to protect the injured party from a foreseeable accident or injury.

Here are a few examples of situations where renters insurance provides coverage if you’re found liable.

Dog and Pet Bites

Dog owners (and other pet owners) are usually held responsible if their dog bites another person. You could also be held liable for other injuries or property damage caused by a dog, such as your dog knocking someone over and causing an injury.

Injured Workers

Someone who's injured while working on your property might sue you if the injury was due to a foreseeable hazard, such as improperly installed air conditioner units or broken lighting.

Slip and Fall Injuries

You can also be held liable for a slip and fall injury that occurs in your apartment if you fail to warn your friend or family member about wet floors, broken railings, or other potential hazards.

In any of these situations, your personal liability coverage can be used to pay for your legal fees and the injured party’s medical payments. You’re only responsible for paying your insurance deductible and any amount that exceeds your liability policy limits.

What’s Not Covered by Personal Liability Insurance

As mentioned above, personal liability coverage in your renters insurance does not extend to intentional injury or damage.

However, there are also some situations where renters insurance does not cover accidental injury and damage, and you require a different type of insurance.

Injury or Damage Resulting From a Home Business

If you run a business out of your home, accidental injury or property damage that results from your work won’t be covered by renters insurance. Instead, you’ll need to purchase professional liability insurance coverage.

Injury or Damage Resulting From Car Use

Liability that results from any accidental bodily injury or property damage caused by the use of your car will be covered by your car insurance.

If you’re a Goodcover member, you can access affordable auto insurance from your Member Dashboard through Goodcover Auto.

Injury Between Two Residents of the Same Apartment

If you live with a roommate and are found liable for injuries they sustain in the apartment, your health insurance will help compensate for their medical expenses. Liability coverage in renters insurance only applies when the claim comes from someone outside your home.

Choosing Your Personal Liability Coverage Limits

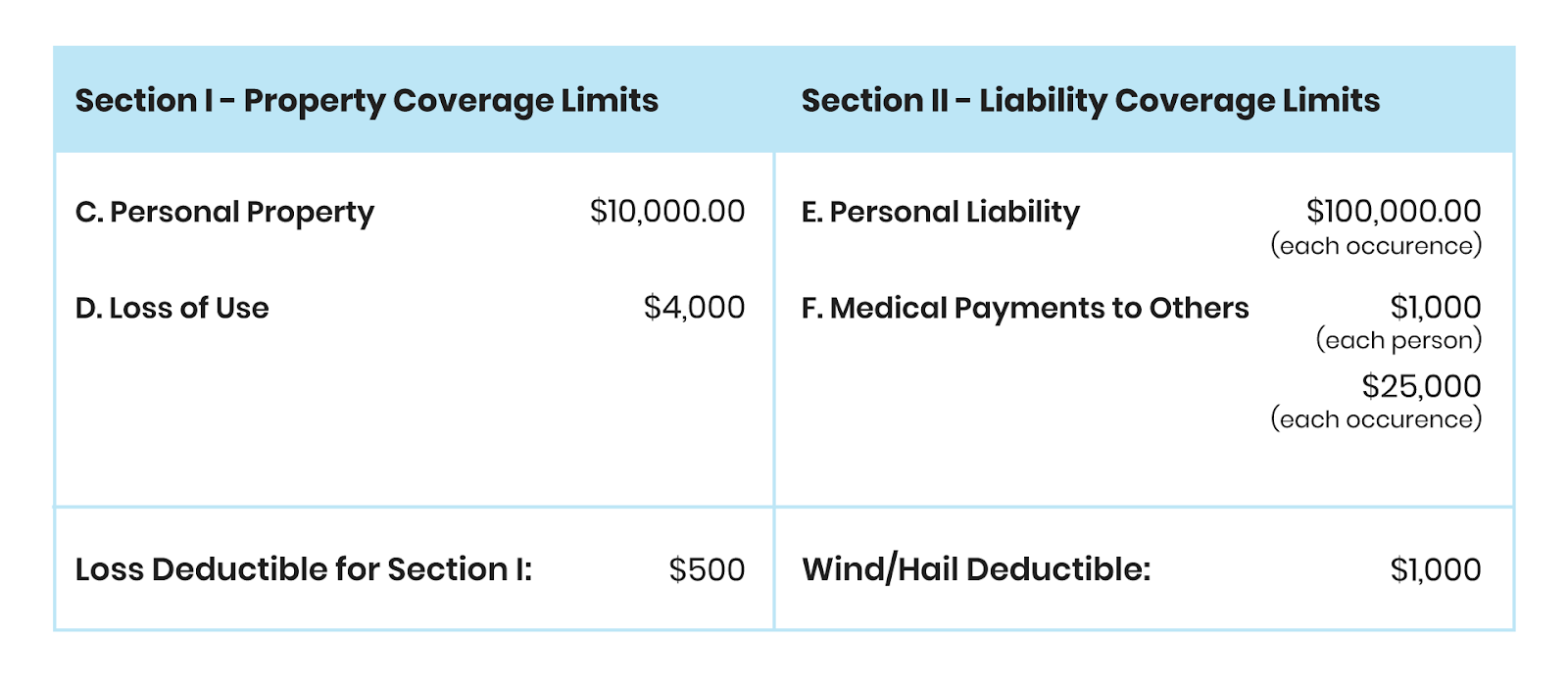

Each type of coverage in your renters insurance policy has a defined limit, the maximum amount of money you can receive for that type of claim. The standard renters insurance liability coverage limit in most cases is $100,000.

For example, limits on your policy might look like:

If your apartment has a low-injury risk, then the standard liability limit may suffice for you. However, you may want to consider additional coverage if you have a dog or an apartment with rickety stairs or poor lighting.

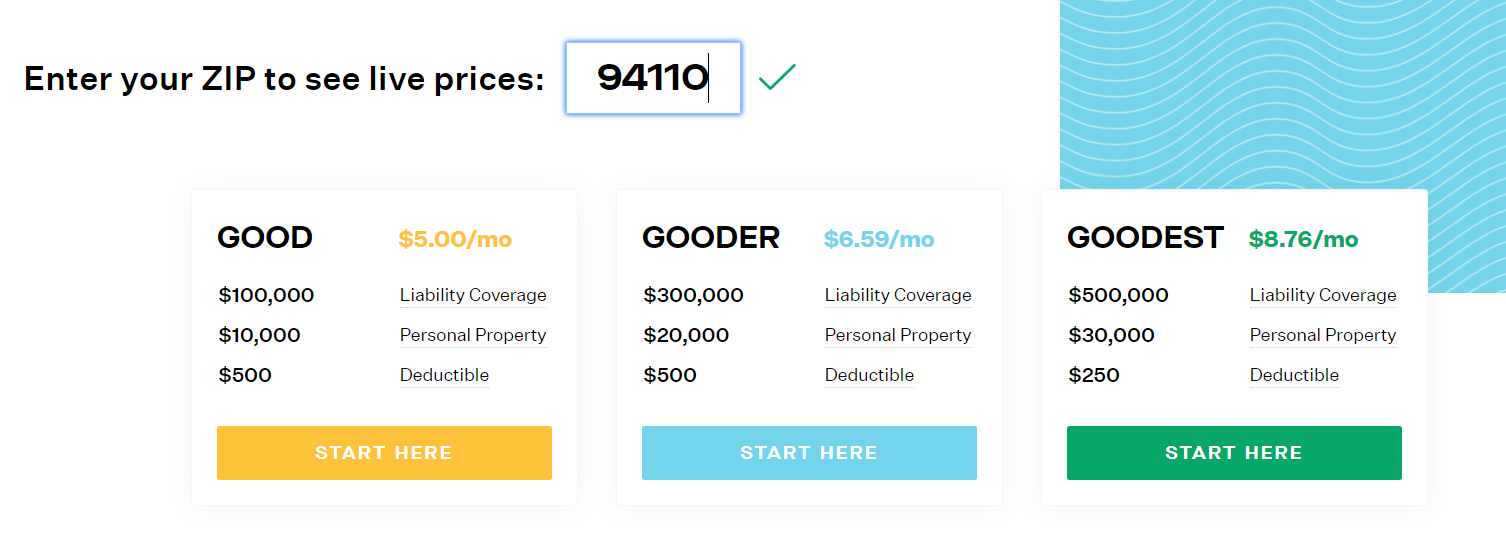

The good news is that renters insurance is highly affordable. Goodcover offers policies starting at just a few dollars per month, and increases in your liability coverage won’t drastically increase your premiums.

However, suppose you want coverage above renters policy limits (~$500,000 or $1,000,000). In that case, you need to speak to your insurance agent about an umbrella policy that covers you and your family members on top of what you get with your renters insurance.

Final Thoughts: What Does Personal Liability in Renters Insurance Cover?

When you move into an apartment building, you should know that your landlord’s insurance doesn’t cover you against liability claims or your belongings against damage.

It helps to have a renters insurance policy.

Renters insurance policies include personal liability coverage that protects you from financial damage if you’re found liable for accidental injury or property damage. It can even pay for your legal fees when you’re not found liable.

Besides personal liability coverage, renters insurance policies offer personal property coverage for your belongings and loss-of-use coverage that helps offset the cost of additional living expenses if your apartment becomes unlivable.

Learn more about the average cost of renters insurance and discover how much coverage is right for you with our Insurance Basics Guide.

Note: This post is meant for informational purposes, insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 15 Aug 2024 • 4 min read

Does Renters Insurance Cover Theft?

Team Goodcover • 1 Aug 2024 • 4 min read

Liability Coverage Explained: What Every Renter Needs to Know

Team Goodcover • 26 Jul 2024 • 6 min read

Colorado Renters Insurance: What You Need to Know

Team Goodcover • 6 Jul 2024 • 6 min read