Goodcover’s Guide To Claim Delays, Denials, and How To Avoid Both

4 Aug 2023 • 7 min read

Suppose you arrive home after a long day at work only to find a pipe burst in your apartment. At first, it’s shocking as you survey the water damage. But then you get a whiff of relief as you remember the renters insurance you purchased.

You have that safety net — now you’re wondering how to file a renters insurance claim.

Filing a renters insurance claim doesn’t have to be complicated, but it can be stressful if not done correctly or if it’s your first time. So let’s help your peace of mind.

This guide will help you understand why renters claims can be denied and how you can influence your claims process to get the highest chances of success.

Let’s dive in.

- How Does a Renters Insurance Claim Work?

- What Can You Claim With Renters Insurance?

- Who Do You Contact for a Renters Insurance Claim?

- How To File a Renters Insurance Claim

- Will Your Insurance Premiums Increase After You File a Claim?

- How Long Does the Assessment Process Take?

- Potential Reasons Your Claim Might Get Denied

- What Should You Do if Your Claim Is Denied?

- Final Thoughts: How To Avoid Renters Insurance Claim Delays and Denials

How Does a Renters Insurance Claim Work?

When you have renters insurance and something bad happens that’s covered by your policy (also known as a covered loss), you can make a renters insurance claim. That’s when you make a formal request to your insurance provider to give you money to help you with what you’ve lost. Once the insurance company validates and approves the claim, you get paid.

After your insurance company reviews your claim, gathers the necessary documents, and decides, you’ll be compensated for anything within the parameters of your renters policy.

If you decide to file a claim, you should do it as soon as possible. Quick action ensures the details stay fresh in your mind, which helps the claim process move forward quickly. Granted, that can be hard when dealing with an unfortunate and stressful accident, but the last thing you want is frustrating delays on your payout.

What Can You Claim With Renters Insurance?

While what’s covered under rental insurance varies, here are some areas most commonly covered:

- Personal property: This commonly includes electronics (such as laptops), clothes, jewelry, musical instruments, and bikes. You can typically claim for damaged items or property loss.

- Personal liability protection: If a visitor gets injured in your home, liability claim coverage can protect you from legal fees and medical bills. Liability coverage typically includes foreseeable events like pet bites, slipping on a wet floor, and other preventable accidents.

- Medical payments to others: If a guest gets injured in your rental unit, this part of your policy covers their medical expenses regardless of who is at fault.

- Additional living expenses: Some covered perils, such as a fire, can leave your residence uninhabitable. That’s called loss of use in the insurance world. Thankfully, renters insurance can cover the costs of temporary housing, meals, laundry, and other essentials.

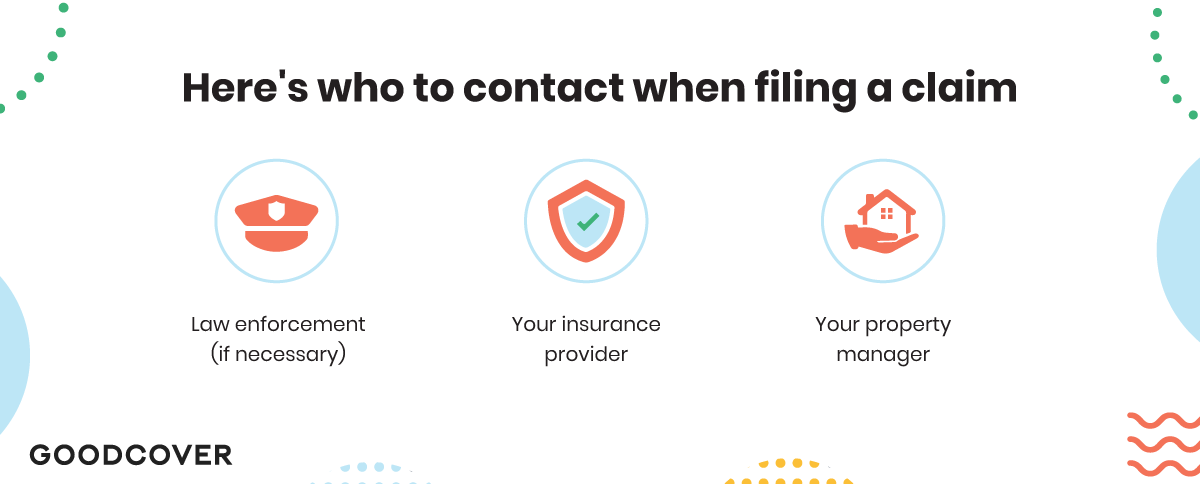

Who Do You Contact for a Renters Insurance Claim?

Regarding how to file a renters insurance claim, the first step is reaching out to the right people — and that would be us if we’re your insurance provider. You’ll need to provide us with details of the incident and the extent of the loss or damage.

If you notice any damage to the structure of your building, let the property manager know right away so they can address the issue. On the other hand, if someone gets seriously hurt, make sure they see a doctor, and keep track of any medical bills.

In scenarios involving theft or vandalism, immediately contact the local police to report the incident — we’ll require a police report to validate your claim.

How To File a Renters Insurance Claim

Filing a renters insurance claim with Goodcover is simple when you follow these steps:

- Document the property damage with photos. Take photographs immediately after an incident or as soon as you discover the damage. Capture images before cleaning, fixing, or moving anything, but prioritize safety if the situation is still dangerous.

- Gather your documentation and communication records. Maintain a folder with the invoices, receipts, text messages, emails, or notes related to your damaged property. Additionally, write a detailed description of the incident so you can accurately relay it to others. Include who was involved, the specifics of what happened, a list of damaged or stolen items (when relevant), the location, and when it occurred.

- Report to authorities and contact Goodcover. In cases where a crime was committed (e.g., theft), contact law enforcement for assistance with a police report. Once you have the necessary documentation to back your claim in hand, contact us.

- Stay proactive and follow up promptly. Remember to communicate openly and return our calls, texts, or emails to keep the process moving and resolve your claim as soon as possible.

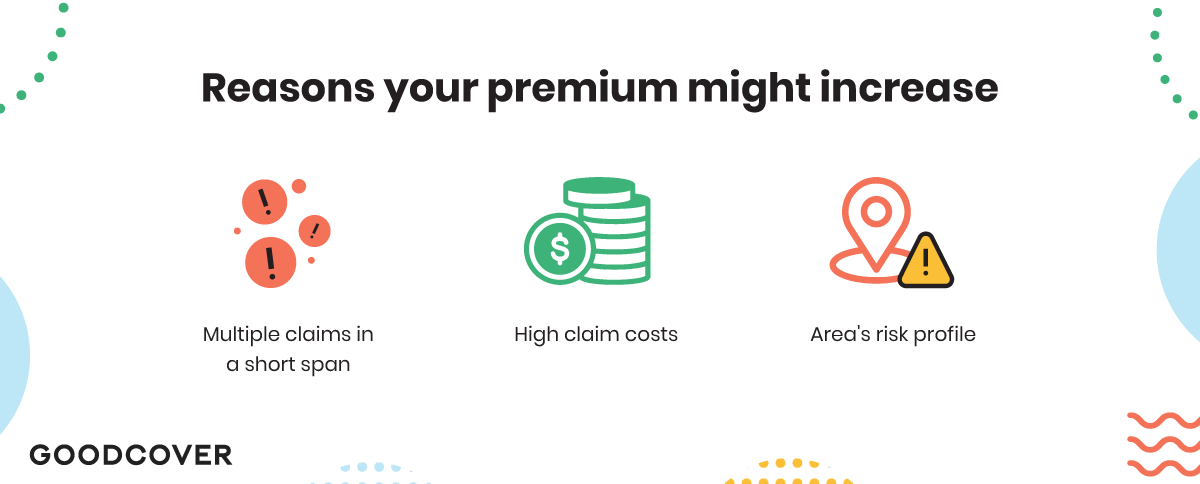

Will Your Insurance Premiums Increase After You File a Claim?

The short answer? It depends. Your premiums may rise if you file multiple claims within a short period or claim particularly costly losses, such as from a big fire.

On the other hand, if you’ve never filed a claim before or an extended time has passed since your last claim, your premiums may remain the same.

As you decide whether to file a claim, consider your unique situation. Sometimes it makes financial sense to handle minor issues out of pocket, especially if your deductible amount is higher or similar to your replacement costs or temporary repairs.

How Long Does the Assessment Process Take?

Typically, insurance claims are processed within 48-72 hours. “Processed” means that the claim is reviewed, acknowledged, and assigned to a claims adjuster.

Then, the settlement process begins. The adjuster oversees investigations and compares that to your renters insurance coverage. They’ll determine who was at fault and look into potential repair costs or medical bills, depending on the type of incident.

This stage is prone to delays between adjusters and policyholders, especially due to poor communication and cooperation. So if you want to get a timely payment, being involved in the claims process and staying proactive and forthcoming with your perspective and documentation is crucial.

When Will You Get Reimbursed?

Depending on the nuances of your situation, you can expect the reimbursement 3-4 weeks after a claim, but sometimes it may be longer. For instance, a claim involving extensive damage or valuable goods can require lengthy paperwork and investigation — thereby extending the time needed for approval.

Once your claim is approved, it can take up to 14 days for funds to appear in your bank account. Remember to be patient and communicative to help — claim adjusters are doing their best.

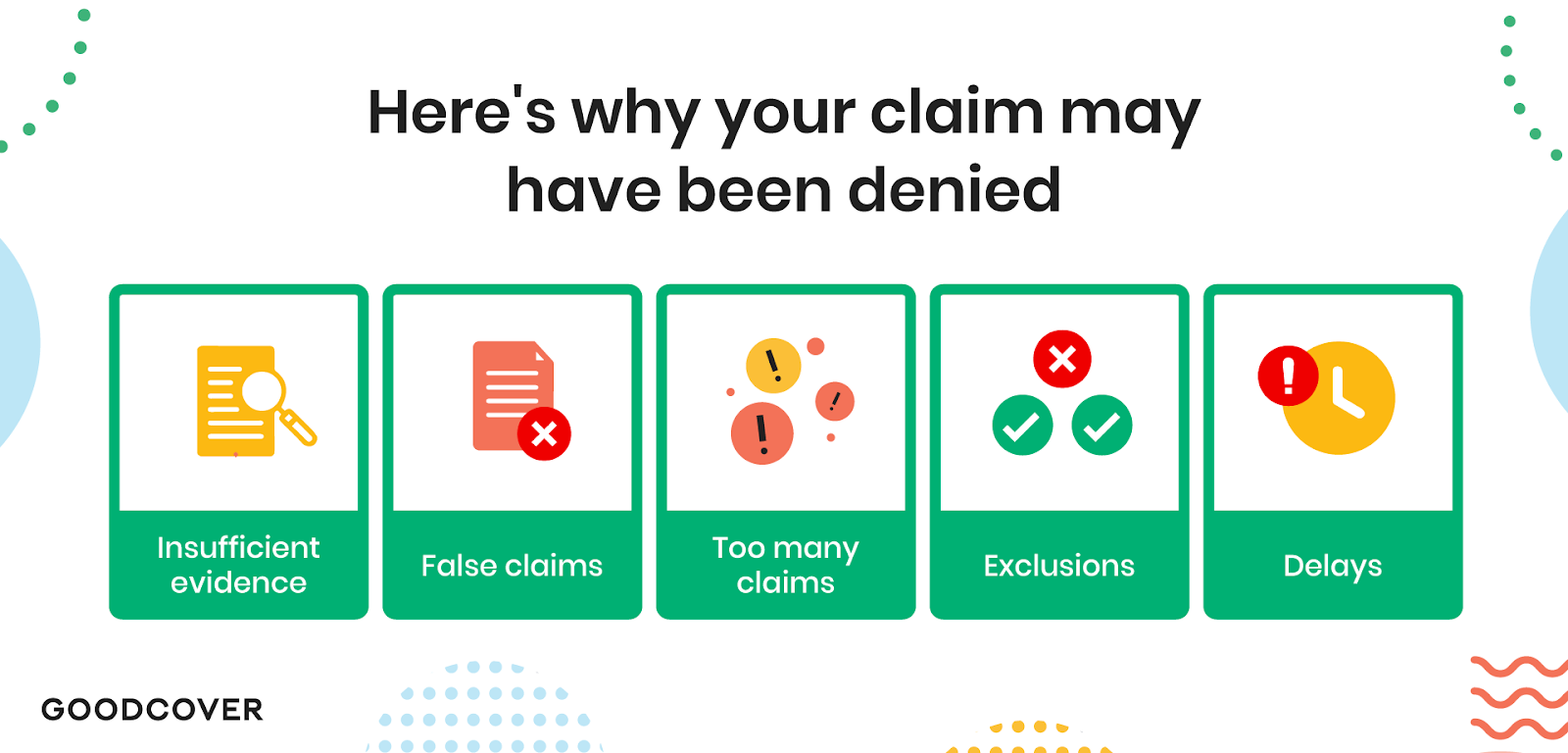

Potential Reasons Your Claim Might Get Denied

Unfortunately, not all renters insurance claims end with you getting paid. You can avoid denied claims by understanding the common reasons why we deny reimbursement.

1. Insufficient Documentation or Evidence

Like other insurers, Goodcover requires sufficient documentation and evidence of damage or theft to avoid fraud. For example, a police report is necessary to verify theft or vandalism claims.

Moreover, save the official versions of documents — a photocopy, screenshot, or picture of a police report will not be accepted due to potential tampering.

You’ll also need documentation proving the actual cash value of your possessions. Otherwise, we may not have the necessary information to deem you eligible for compensation.

To make sure you get reimbursed for the right amount, create a home inventory. Find and store the receipt proving the value of your possessions. If anything is later damaged or stolen, you can easily bring out the receipts to substantiate your claim and get your payout faster.

2. False or Exaggerated Claims

The insurance industry invests millions of dollars into fraud detection. Submitting false or exaggerated claims is unethical and could lead to denial, policy cancellation, and legal consequences. It’s always best to stay honest in your claims and filings.

3. Frequent Claims in a Short Timeframe

If you file multiple claims within a short period, insurers may become suspicious or view you as high-risk — particularly if the underwriter suspects fraud.

If you have to file consecutive claims, try to provide as much information, documentation, and proof as possible. It’ll help both you and us achieve the best outcome.

4. Exclusions in Your Policy

If your claim involves damages that fall under the exclusions in your Goodcover policy, it's likely to be denied (e.g., car theft, impossible-to-insure events, and costs of moving).

Knowing the intricacies of your plan will help you avoid getting denied. And if you have concerns about specific events, you can always discuss additional coverage with Goodcover’s Member Experience team or your alternate insurance provider.

5. Communication Delays

Any delay in communication can hinder the claims process and possibly result in denial.

Even third parties must stay in the loop. Whether it’s contractors, another person’s insurance company, hospital staff, police, or your property management company, they will likely be asked to chime in.

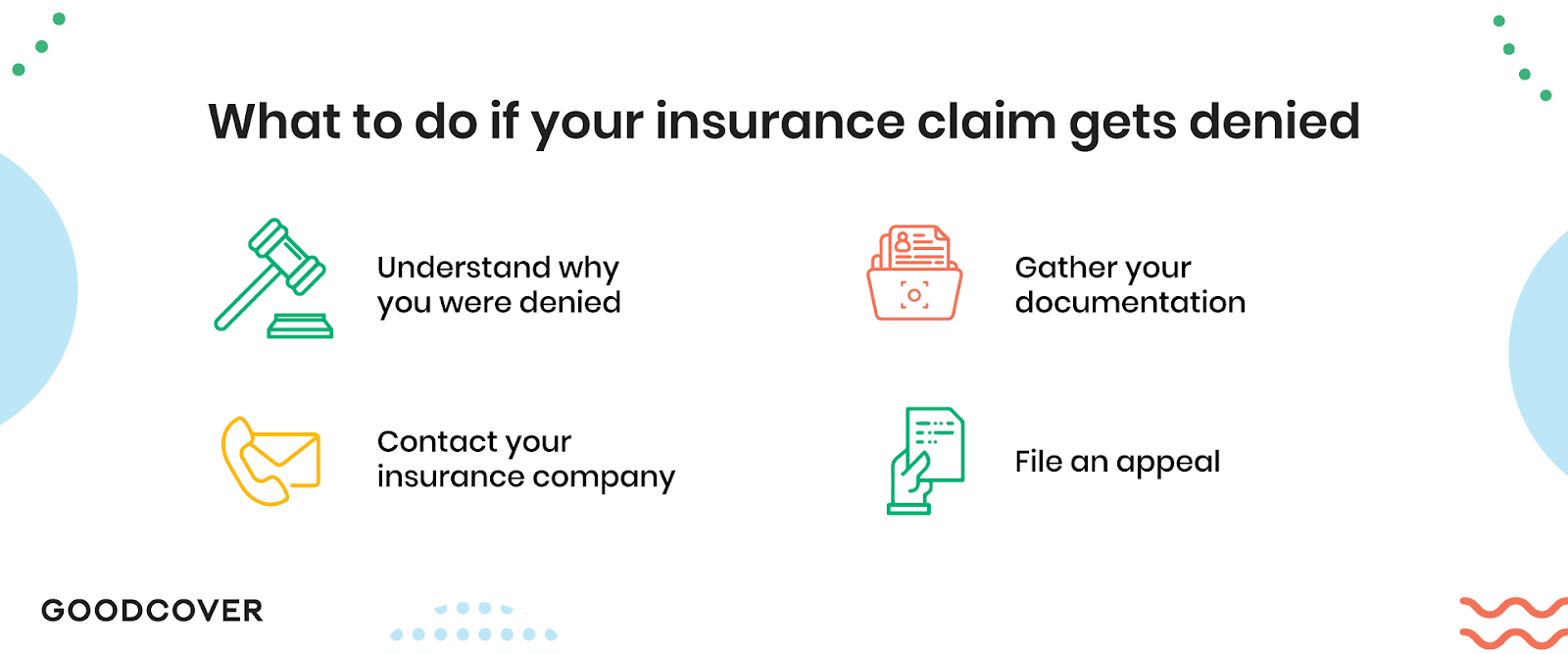

What Should You Do if Your Claim Is Denied?

If your claim gets denied, the first step is understanding why. You can start by meticulously reviewing the denial letter, which should include an explanation.

If you believe the denial resulted from a missing document or an error, you can fix the issue and resubmit your claim with the correct information.

If you think the denial was unjustified or based on an error on our part, consider submitting a formal appeal. In that case, document your case thoroughly and be prepared to present supporting evidence.

Final Thoughts: How To Avoid Renters Insurance Claim Delays and Denials

While filing a renters insurance claim can seem overwhelming, the process can be straightforward when you’re informed, proactive, and forthcoming with information.

Now that you understand why claims get delayed or denied, you’re more likely to submit a claim that goes smoothly and favorably.

You can prepare in advance by reviewing your current renters insurance policy. If you’re unhappy with its coverage, get a renters insurance quote for a Goodcover plan. We’ll cancel your old policy for you, even if you’re on an annual contract.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 24 Nov 2023 • 5 min read

Everything You Need To Know About the Renters Insurance Claim Process

Team Goodcover • 25 Aug 2023 • 6 min read