The Comprehensive Guide to Understanding How Renters Insurance Pays Out

25 Aug 2023 • 6 min read

Imagine you've just returned home to a devastated apartment — a fire turned your cozy space into a burnt mess. Your heart sinks as you realize your expensive electronics, furniture, and personal items are ruined.

Thankfully, you’re insured. But how much will your renters insurance cover? And how much will your renters insurance payout be?

Understanding Goodcover’s claims process will help ensure you get the most out of your insurance policy, and this article will cover everything you need to know.

- What Are the Types of Coverage Offered by Renters Insurance?

- How Do Insurance Companies Determine an Item’s Value?

- How Do Policy Limits Work?

- Payouts for Shared Property

- How Long Does It Take For Renters Insurance To Pay Out?

- How Does Renters Insurance Payout Work, and When Will You Receive It?

- Final Thoughts: How Does Insurance Determine What To Pay You

What Are the Types of Coverage Offered by Renters Insurance?

Renters insurance can be a financial lifeline when you face unexpected events like theft, fires, or someone suffering an injury in your home. So it's crucial to understand the different types and what they cover.

Personal Property Coverage

Personal property coverage is the most common type of coverage you think of when you think of renters insurance. This covers the cost to repair or replace your personal belongings, like furniture, clothing, and electronics, if stolen or damaged. However, certain item classes, like jewelry, may have limited coverage or require additional coverage.

Liability Coverage

Personal liability coverage protects you if you are found legally responsible for causing bodily injury or property damage to others. For example, if someone were to slip and fall inside your apartment and sue you, filing a liability claim could help cover the legal costs and any potential settlements.

Temporary Housing Coverage

Temporary housing coverage, also known as loss of use, kicks in when a covered loss makes your rental unit uninhabitable. During repairs to your rental unit, this coverage can help pay for additional living expenses like hotel stays or extra costs from a longer work commute.

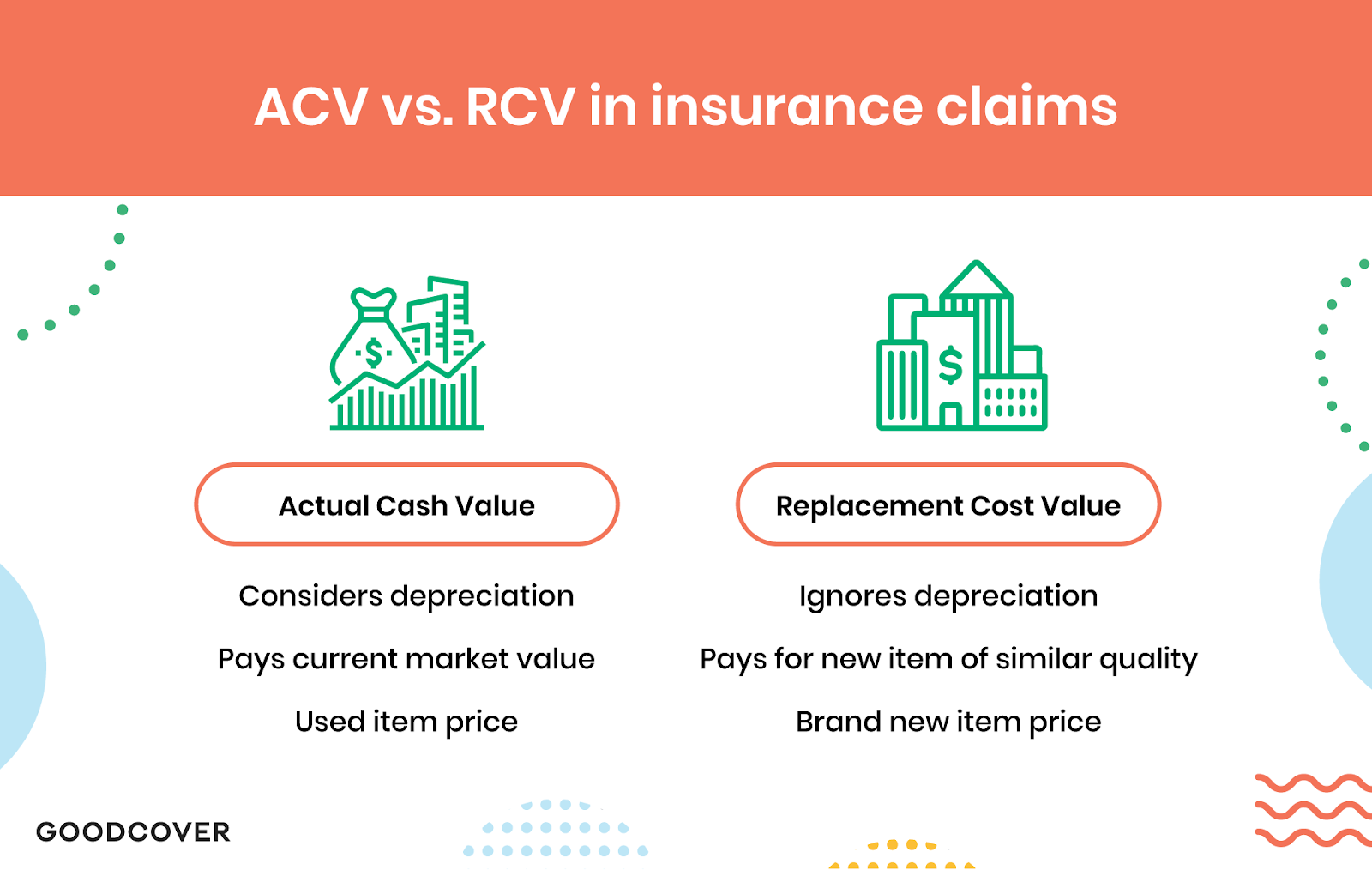

How Do Insurance Companies Determine an Item’s Value?

Insurance shouldn’t be a guessing game, so let’s give you a clear picture of how the value of your stuff is determined.

Insurance companies mainly use two methods for valuation: Actual Cash Value (ACV) and Replacement Cost Value (RCV).

ACV is a “used item” cost. In other words, if your insurance company uses this valuation, they’ll look at the current value of your item and factor in depreciation. So if your five-year-old laptop was stolen, ACV would cover its current value, which would be less than the original price you paid, due to depreciation.

In contrast, Goodcover uses RCV on all its insurance policies. RCV is the “new item” price, and is based on the cost of replacing your item with a new one of similar quality. Using the same example of the stolen laptop, RCV would cover the cost of buying a new laptop with equivalent features.

Goodcover Members enjoy RCV coverage on all personal belongings. That helps ensure you can replace your possessions without worrying about depreciation reducing your renters insurance claim payout.

How Do Policy Limits Work?

When reading through your renters policy, you’ll notice policy limit amounts. Think of these as safety nets, but with a maximum amount of money they can catch. Policy limits dictate the maximum dollar amount for any renters insurance claim payout in each category.

For example, Goodcover’s standard plan covers perils like theft, fires, or water damage after a deductible but excludes accidental damage. And you can easily adjust for special items like an expensive bike or wedding ring from the member dashboard.

Goodcover also offers SUPERGOOD extended coverage with enhanced policy limits and accidental damage for specific item classes (i.e., jewelry, musical instruments, and cameras).

Under Goodcover’s SUPERGOOD plan, extended coverage broadens your policy limits for these items and provides additional deductible-free coverage.

Additionally, you need to think about categories when applying for extended coverage. Depending on what category your valuable items fall into, that’s how you’ll choose your coverage.

Also, make sure the sum of your possessions in a category significantly surpasses the standard limit, ensuring extended coverage is a sensible investment for you.

Payouts for Shared Property

If you and your roommate invested in a quality, expensive sofa that got damaged and you don't share the same policy, things can get tricky. Because you bought the sofa together, your renters insurance claim payout might not be what you expect.

Payouts for shared property often mirror your ownership share. In this instance, assume your ownership was 50%, and if your claim was approved, you’d receive 50% of the claim valuation as your payout.

However, at Goodcover, we let Members share a single renters insurance with roommates. That way, you won’t need to deal with the headache of shared property payouts and reap the benefits of splitting the costs, including the deductible when you file a claim.

How Long Does It Take For Renters Insurance To Pay Out?

Your renters insurance claim payout may take anywhere from one month to arrive or longer, depending on the complexity of your claim.

How Does Renters Insurance Payout Work, and When Will You Receive It?

When calamity strikes, you may get curious about the behind-the-scenes work on your claim. And more importantly, when you’ll receive your settlement.

Here’s how a claims adjuster (an employee who assesses the facts surrounding a claim) determines your payout and when you receive it:

1. Filing a Claim

After a loss, you’ll first need to file a claim form with your insurance company. Then, you’ll need to substantiate your claim. Provide all the essential details: what happened, the extent of the damage, and any documentation (e.g., a home inventory of personal belongings) that supports your claim.

2. Claims Adjuster Assignment

Next, your insurance company will assign a claims adjuster to review your ticket. They’ll analyze your insurance policy to see what's covered and carefully review your provided documentation.

3. Initial Contact

After they’ve looked at the initial claim, your adjuster will likely reach out to you to discuss your claim and policy. Take this opportunity to clarify any uncertainties regarding your claim because your adjuster is on the same team as you.

4. Investigation and Damage Evaluation

Then, the adjuster begins a thorough investigation. For instance, if you’re filing a claim for burglary, they’ll look at the police report and evaluate the evidence. They’ll also decide the value of the damage caused by the event.

In the case of a burglary, the adjuster will use your evidence, the police report, and your proof of ownership. You should be fully prepared to share receipts and photos of your stolen or damaged property. They also might ask to visit your place and take pictures to help estimate the reimbursement or repair costs in cases where there’s large damage.

5. Policy Evaluation

The adjuster reviews your policy limits and deductibles to determine how much the insurance company will pay. If your policy covers $15,000 for water damage, and the burst pipe caused $10,000 worth of damage, that’s within the coverage limits. But if an expensive painting was ruined, that might be over the single-item limit.

That’s where having extended insurance coverage or Goodcover’s SUPERGOOD plan provides immense benefits for valuable items.

6. Payout Decision and Settlement

Once the adjuster has gathered all the details and done the math, it’s time for a decision. If your claim is approved, they’ll calculate the payout amount based on policy terms and your losses.

Once approved, a settlement is proposed. If you agree with the payout, you'll sign the documents, and the insurance company will process the payment. After receiving your signature, it may take up to two weeks to receive your check or ACH direct deposit.

Final Thoughts: How Does Insurance Determine What To Pay You

While it may seem trivial, becoming savvy with renters insurance policy coverage limits and terms will help you choose the best one for you and help you maximize your renters insurance claim payout. You’ll know exactly which damaged items should be covered and roughly how much your payout will likely be.

If you’re still deciding between renters insurance providers, check out Goodcover. Compare and switch today to save on renters insurance.

Note: This post is for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 16 Aug 2024 • 2 min read

Goodcover Weekly Recap | Week of August 11, 2024

Team Goodcover • 9 Aug 2024 • 2 min read

Goodcover Weekly Recap | Week of August 4, 2024

Team Goodcover • 26 Jun 2024 • 8 min read

How to Get Renters Insurance

Team Goodcover • 13 Jun 2024 • 6 min read