A Renter’s Guide to Credit Checks: How It Works

1 May 2024 • 7 min read

Looking for apartments can feel like a roller-coaster ride. There's the thrill of new beginnings but also the knot in the pit of your stomach when it comes to the details — like credit checks.

The thought of someone running your credit can be scary, especially when you're not sure what your credit report might reveal.

Navigating rental applications means taking a hard look at your financial health—your credit score, income level, and current expenses. Most landlords won't just hand you a key based on good vibes and a handshake; they want to make sure you can pay your bills on time.

But what are the details of a renters credit check? Does renters insurance affect your credit score? When will your credit be checked, and will it happen more than once? And what is a good credit score for a tenant to have?

By understanding your financial health, you can make a favorable impression to help secure that bigger place you’ve been eyeing.

We’ll walk you through the details of credit scores and renting, plus tips on raising your credit score.

- Why Do Landlords Check Your Credit Score?

- How To Provide Proof of Income

- What’s a Good Credit Score?

- How to Improve Your Credit Score

- The Impact of Late Rent on Your Credit Score

- How to Rebuild Your Financial Health

- Final Thoughts: Does Renters Insurance Affect Your Credit Score?

Why Do Landlords Check Your Credit Score?

Typically, tenant screening processes like credit reports and criminal background checks are done to determine whether you can and will pay your rent on time. Credit reports paint a general picture of whether you pay on time.

While a credit score isn’t the full picture of your financial health (such as being unemployed or if a parent is helping pay your rent), a tenant credit check is the primary way for landlords and property managers to vet you and check for items like a past bankruptcy.

For example, on-time payments and a positive rental history show you are more likely to pay your new landlord on time. On the other hand, late credit card payments could show the landlord that you might be late on payments or just not pay at all.

Fortunately, your credit score is only checked once at the beginning of the renting process, and the Fair Credit Reporting Act protects your information.

It only affects getting the lease, not the amount of your rent, so your rent won’t be affected by a score decrease to poor credit midway through your lease if you run into difficulty. That also means your credit score doesn’t affect renters insurance premiums, although on-time payments can help your score.

How To Provide Proof of Income

In addition to paying on time, a potential tenant screening report usually asks for proof of income to compare against your renter's credit check information. Landlords usually want proof of income showing at least three times more than your proposed rent.

They want to avoid tenants being rent-burdened, which means their total housing costs exceed 30% of their gross income. When tenants spend too much of their income on rent, they face hardships that can force them to choose between paying other bills and rent.

How you provide proof may vary based on the tenant screening service your landlord uses. However, you can usually provide proof of income through copies of your paycheck stubs, previous year's income tax returns, or bank account statements. If someone is helping you make payments, you’ll also need proof of their income.

If you are between jobs and need to move, explaining the situation and providing extra proof of previous income can help. For example, you might share tax returns from several years to show a pattern of income.

Or you might show that you work in a seasonal industry, like teaching, to explain the current situation. Like a security deposit, the goal is to reassure the landlord.

What Credit Score Do You Need To Rent an Apartment?

Every landlord has their own target credit score and uses different reporting agencies to get tenants’ credit reports. However, a 700 FICO score is generally considered “good credit.” Experian, TransUnion, and Equifax, the three major credit bureaus, use scales ranging from around 300 to 850 for credit scores. In 2023, the average score was 715.

Landlords in competitive rental markets tend to favor renters with higher scores, hoping to avoid prospective tenant evictions. So, while bad credit might not affect rent prices, it can make it harder to get a lease.

How To Improve Your Credit Score for Renting

While score building can take months or years, there are ways to speed up the process.

Use a credit-building service

Credit-building tools like secured credit cards and credit-builder loans are designed to help you establish a positive credit history. Secured credit cards let you deposit money as collateral, and the card issuer reports your payments to the credit bureaus.

Similarly, credit-builder loans work like this: you make regular payments into a savings account, and once your loan is paid off, you can access the money you've paid into the account.

Keep balances low

Slash your interest charges and boost your credit score by keeping your credit card balances low. Maintaining a low credit utilization ratio – the amount of credit you’ve used compared to your total available credit – is important because it’s a metric that makes up about 20% of your TransUnion score.

For example, if you have a credit card with a $3,000 limit and a $1,000 balance, your credit utilization is 33%. Most experts recommend keeping your credit utilization below 30%.

Limit new credit and hard inquiries

When a potential lender checks your credit, it’s called a hard inquiry. Too many hard inquiries in a short time can suggest you might be taking on too much debt, lowering your score. Soft inquiries, like checking your own credit score or a company pre-qualifying you for an offer, don’t impact your score.

Understanding your credit score is important. Here are the five main factors that determine it:

- Payment history: Your record of on-time payments.

- Credit age: How long you’ve had credit accounts open.

- Utilization: How much credit you use vs. how much you have available.

- Balances: The total amount you owe across all loans and credit cards.

- Number of credit lines: The mix of credit accounts you have (how many credit cards, how many loans, etc.)

Stay consistent

Payment history is typically the largest credit score factor, so pay on time, every time. Just a single late payment can lower your credit score and stay on your credit report for up to seven years. And remember, being late or skipping payments on your student loans counts against your credit.

Can Late Rent Payments Hurt Your Credit Score?

Rent payments may not have affected your credit score in the past, but that’s changed. Landlords can now report missed or chronically late rent payments to the credit bureaus, potentially causing a significant drop in your score.

While there are services that help you report on-time rent payments to boost your credit, the reverse is also true – landlords can now report late or missing payments, potentially hurting your credit.

How To Avoid Late Payments

Avoiding late payments is your best defense to protect your credit score. Here are some tips to avoid late payments:

- Set up automatic rent payments through your bank or a rental payment platform.

- Create a budget that prioritizes your rent payment.

- If you are facing financial difficulties, talk to your landlord immediately to discuss options.

- Explore local or state rental assistance programs if you experience hardship.

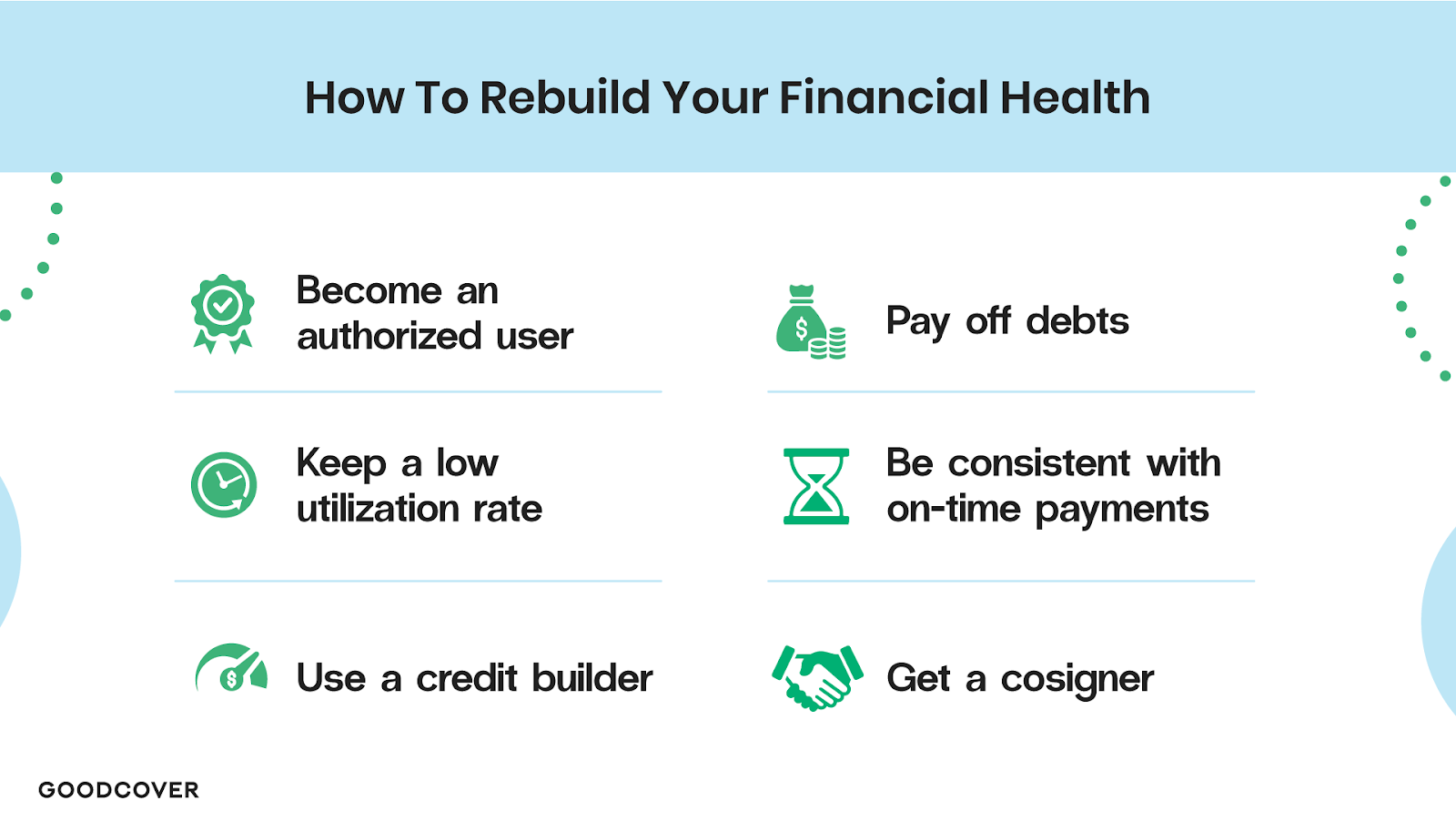

How To Rebuild Your Financial Health

Your credit score is just one part of your financial situation. Emergency funds, debt, and asset protection all affect your financial health.

Here are some ways to rebuild your credit and overall financial health:

Become an authorized user: If you have a family member with good credit, you can ask if you can be an authorized user on one of their credit cards, which can boost your credit score by adding additional history.

Pay off debts: Focus on paying down your debt, starting with high-interest accounts like credit cards.

Keep a low utilization rate: The lower, the better, but anything below a 30% utilization rate is acceptable.

Be consistent with on-time payments: Make all your payments on time, every time.

Use a credit builder: Consider using a credit-builder loan or secured credit card to prove your creditworthiness and boost your score.

Get a cosigner: If you're having trouble qualifying for credit on your own, ask a family member or friend with good credit to cosign for you. This can help you start building a credit history.

Final Thoughts: Does Renters Insurance Affect Your Credit Score?

While renters insurance only impacts your credit score in terms of whether or not your payments are on time, it can help show responsibility to landlords when paired with a good credit score. Working together, those two items can help you secure a lease.

By understanding how renters credit checks work and proactively improving your financial health, you can become a more attractive tenant and protect your belongings with a comprehensive renters insurance policy.

At Goodcover, we offer affordable, transparent renters insurance policies that provide the coverage you need without hassle.

Get a quote today and enjoy the peace of mind that comes with knowing your possessions are protected.

Note: This post is meant for informational purposes, insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 2 Jul 2025 • 16 min read

Affordable Renters Insurance in Sacramento, CA

Team Goodcover • 23 Jun 2023 • 6 min read

The Ultimate Rental Inspection Checklist for Tenants

Team Goodcover • 9 Jun 2023 • 6 min read

Beyond Packing: Goodcover’s Tips for Moving Out Efficiently

Team Goodcover • 21 Apr 2023 • 6 min read

How Tenants Can Avoid Rental Scams: 4 Things To Keep in Mind

Team Goodcover • 17 Feb 2023 • 7 min read