Your Ultimate Guide to Arizona Renters Insurance

1 Aug 2022 • 6 min read

Arizona is home to some of the most breathtaking landscapes in the country — the Grand Canyon's just the beginning. This state has everything from beautiful sunsets to sprawling desert scenery and cuisine that would make any foodie salivate.

However, Arizona is prone to natural disasters like wildfires, flash floods, and thunderstorms. For instance, in 2023, there were approximately 1,659 wildfires reported, with 176,939 acres burned. And in 2024, Arizona wildfire activity is trending even higher.

On top of that, Arizona has a higher property crime rate than most other states. Safewise shares that property crime increased by nearly 24% year-over-year, despite a nationwide decrease of 7%.

With such data, it’s no surprise that Arizonans are more proactive about home security than most American families.

One way to protect yourself is having a renters insurance policy, which covers your personal belongings in the event of a covered loss.

Keep reading to discover:

- Is Renters Insurance Legally Required in Arizona?

- Average Arizona Renters Insurance Cost

- What Does Renters Insurance Cover in Arizona?

- What Does Renters Insurance Protect Against?

- Top Arizona Renters Resources for Tenants

Is Renters Insurance Legally Required in Arizona?

There's no law requiring Arizona tenants to have renters insurance. But sometimes, landlords may require it as a condition for moving in. A renters insurance policy will cover your losses if the building burns down, so that’s a good incentive for your landlord to request it.

Even if your landlord doesn't need you to have renters insurance, it's a good idea to purchase a policy anyway. Renters insurance is an affordable way to protect your personal property and avoid a heavy financial burden if something unexpected happens.

Some Arizona tenants misunderstand who’s responsible for their personal belongings if there’s a fire or theft. It’s always the tenant, never the landlord. The landlord isn't accountable for your personal possessions. Your stuff, your responsibility.

That’s why it’s a good idea to cover your belongings with renters insurance. It’s inexpensive — with Goodcover, plans are affordable — and the coverage will reimburse the cost to replace your items, not just the actual cash value of what it’s worth today. That means that if someone steals your 2014 laptop, you'll get paid the necessary funds to cover its replacement today, not what your 2014 laptop is worth today (which probably isn’t much).

Do I Need To Add My Landlord to My Policy?

Your landlord may request to be added as an additional interest on your renters insurance policy because they want your insurance to notify them if you cancel your policy or make any changes.

For example, some tenants will sign up for renters insurance, show proof to the landlord, then cancel the policy the next day. Having your landlord as additional interest will notify them immediately of this lease violation, allowing them to take corrective action and ensure their interests are protected.

If your landlord wants you to name them on your renters insurance policy, clarify whether they mean additional interest or additional insured.

As an additional interested party, they'll only see the policy and any changes you make to it, but they can't make the changes themselves.

If the landlord means additional insured, our customer support team will gladly send you a letter explaining why your landlord shouldn't be additional insured on your policy.

Should I Add a Roommate or Significant Other?

Currently, you can’t add your roommate to your renters insurance coverage, but they can and should get their own affordable policy. Adding your significant other is a straightforward process, though.

If you add your significant other as named insured, they'll be covered by the insurance policy and can make changes. For example, if a kitchen fire destroys your furniture, your significant other will also be compensated as a policyholder.

You also won’t need to worry about disclosing the nature of your relationship to additional interests in your policy (e.g., your landlord). So, you’ll be safe from anti-LGBT+ and discriminatory housing policies.

Average Arizona Renters Insurance Cost

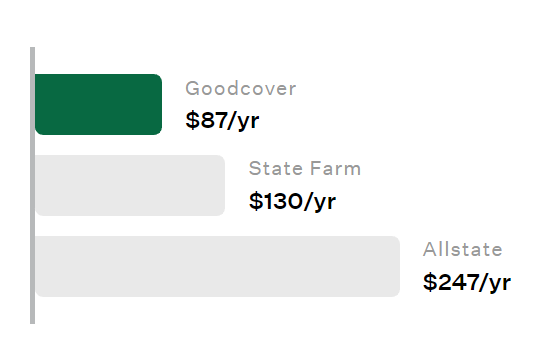

The average cost of renters insurance in Arizona is $211 per year ($18 per month).

Renter’s insurance companies like State Farm and Allstate cost $130 and $247 per year. But Goodcover offers more affordable premium costs.

That said, prices vary greatly. Your location, deductible, coverage amount, and claims history can impact renters insurance costs.

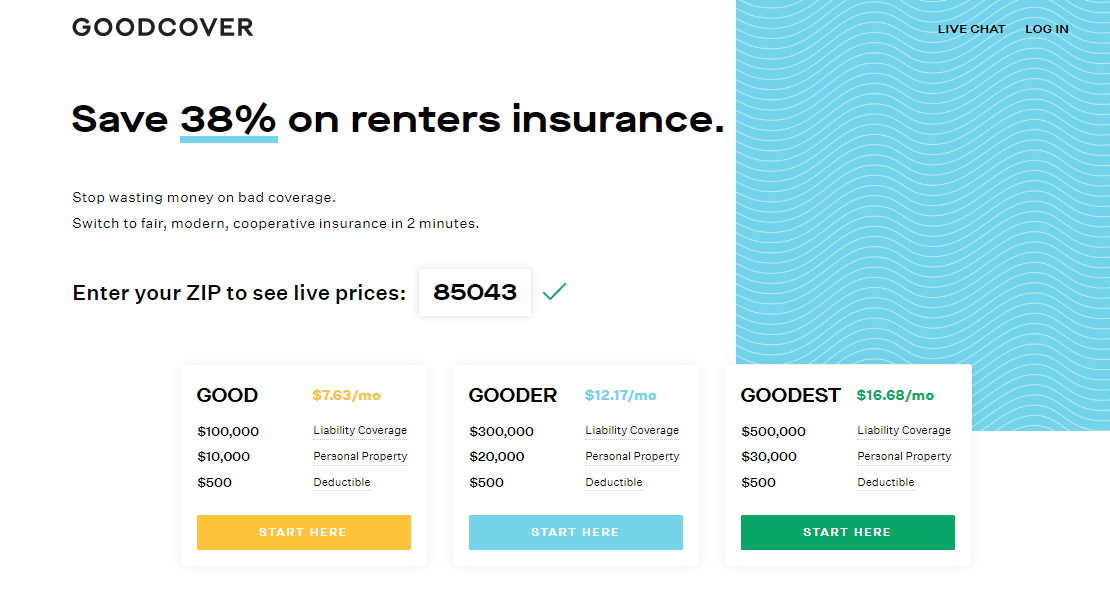

For example, suppose you recently moved to Phoenix, and your zip code is 85043. In that case, your renters insurance policy will start at $7.63 per month.

Goodcover also returns any unclaimed premiums to its Members through the Goodcover Member Dividend. For example, Goodcover returned 1.93% of the collected premiums to Members in 2021.

What Does Renters Insurance Cover in Arizona?

Renters insurance has three components: personal property, liability coverage, and temporary housing.

Personal property coverage protects your personal belongings. Even if you have a minimalist lifestyle, you might be surprised at the value of your possessions.

Replacing all these items in the event of a fire or other disaster could push you into bankruptcy. Renters insurance can enable you to get back on your feet by helping you replace all your lost items.

You could also be held responsible if an accident happens on your rental property. That wet floor or icy stairs might seem inconsequential, but if someone slips and falls, they can sue you to cover their medical payments.

Personal liability coverage covers the injured party's medical expenses in such cases. Liability coverage also ensures you’re not liable to the landlord if you cause property damage.

If your apartment becomes unlivable, temporary housing coverage (loss of use) will help cover your additional living expenses. However, this coverage only applies if your apartment becomes uncomfortable to live in due to a covered peril — one of the losses covered by your renters policy.

For example, if your apartment in Phoenix burns down, living in a hotel in the city would be costly. Eating out every night would also increase the bill. If you have renters insurance, your policy covers these expenses up to your coverage limits while reconstruction occurs.

What Does Renters Insurance Protect Against?

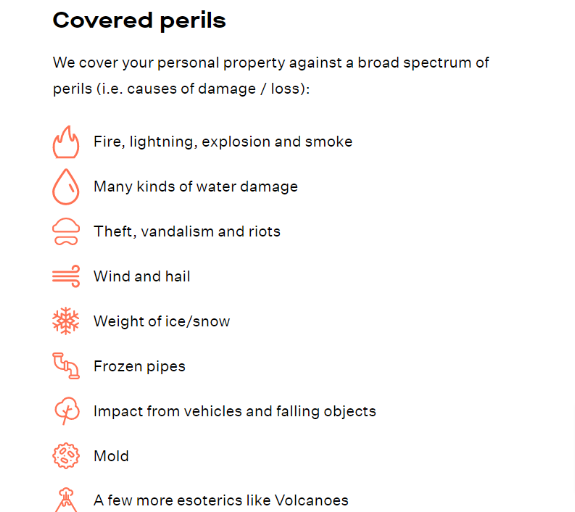

Renters insurance in Arizona typically protects you against fire, lightning, explosions, and water damage. It also covers you against theft, burglary, and vandalism.

Renters insurance from Goodcover can also cover accidental damage with our SUPERGOOD package, which costs only a few more dollars per month. So, if you accidentally spill pool water on your laptop and damage it, you can file a claim and receive compensation. That's good coverage!

Top Arizona Renters Resources for Tenants

We believe that knowledge empowers individuals to make the best decisions in life.

To that end, we've compiled the following resources for tenants in Arizona:

- Renters Rights in Arizona

- Your Rights as Arizona Tenant

- Resources for Renters in Arizona

- Organizations Providing Affordable Rentals

If you’re planning to rent in Arizona but are unsure how much Goodcover can save you on your renters insurance in AZ, get a renters insurance quote in a few seconds.

Or, if you have an existing renters insurance policy, email compare@goodcover.com and we’ll compare your rates to ours. If you like what you see and are ready to switch, we’ll cancel the old policy for you and refund anything you prepaid.

And now finding the best car insurance rates just got easier with Goodcover Auto. This new service helps you quickly find rates from multiple leading insurers to help you compare prices and coverage to pair with your renters insurance policy.

Note: This post is meant for informational purposes, insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 15 Jul 2025 • 16 min read

Does Renters Insurance Cover Theft? A Simple Guide

Dan Di Spaltro • 14 Jul 2025 • 15 min read

Commercial Insurance for Rental Properties: Landlord Guide

Dan Di Spaltro • 11 Jul 2025 • 19 min read

Cheapest Renters Insurance in NJ: A Guide to Affordable Coverage

Dan Di Spaltro • 10 Jul 2025 • 13 min read

Best Renters Insurance in Milwaukee: Your Guide to Coverage

Dan Di Spaltro • 8 Jul 2025 • 14 min read