Should You Cancel Renters Insurance During a Recession? Here’s What To Do Instead

10 Mar 2023 • 6 min read

Are you finding affording rent and your other expenses challenging right now? Many people are — in 2022, the average American household spent 30% of its income on rent.

And with the possibility of a recession, you may be stressed about making ends meet if you lose your job. In January 2023 alone, 50,000 employees lost their jobs, largely due to the surge in tech layoffs.

We understand that in difficult times it's natural to cut back on unnecessary expenses and save money. But your renters insurance policy isn't a luxury; it’s a necessity.

For just a few dollars every month, you could potentially save yourself and your family from losing everything in a catastrophe — just by having an adequate renters insurance policy.

Without renters insurance coverage, you might find it hard to replace personal items if something unfortunate happens. Or you might be held liable for someone’s injuries if they got hurt at your place.

Just think about it:

If someone robs you or your neighbor’s leak causes flooding in your apartment, do you really want to get stuck replacing everything out of your own pocket? That’s what will happen without proper insurance coverage. So let's see how you can make the most of your renters policy during these challenging times without sacrificing protection.

- If a Recession Hits, Should You Cancel Your Renters Insurance Policy?

- What Happens if I Cancel My Renters Insurance?

- What To Do Instead of Canceling Your Renters Insurance Policy?

- Additional Perks of Having a Renters Insurance Policy

- Final Thoughts: Should You Cancel Renters Insurance During a Recession?

If a Recession Hits, Should You Cancel Your Renters Insurance Policy?

In short, no.

It might save money in the short term, but canceling your renters policy could cost you more in the long run.

Without insurance coverage, you’re putting yourself at high financial risk from property loss and personal liability.

Just look at the many damages that pose a risk to your personal property:

Without a renters policy, you'd face replacing potentially thousands of dollars worth of personal property on your own. And if there was an injury to someone else, the costs could skyrocket quickly.

Simply put, keep your renters insurance policy – it’s worth it!

What Happens if I Cancel My Renters Insurance?

When you cancel your renters insurance policy, you lose protection immediately on the cancellation date. And depending on the cancellation policy, you may be due a partial refund of your premiums minus any cancellation fees.

Keep in mind that if your landlord requires renters insurance as part of the lease agreement, you could get evicted from the property without current coverage.

If your landlord is listed on your renters insurance policy as an additional interest, they'll be notified when you make changes to your policy or if your policy becomes inactive. Keeping your renters policy can help you stay in your home.

What To Do Instead of Canceling Your Renters Insurance Policy?

Canceling your renters insurance leaves you at risk and is almost always the least desirable option for renters. The good news is you can take action and get more bang for your buck instead of canceling your renters insurance policy.

Here’s how:

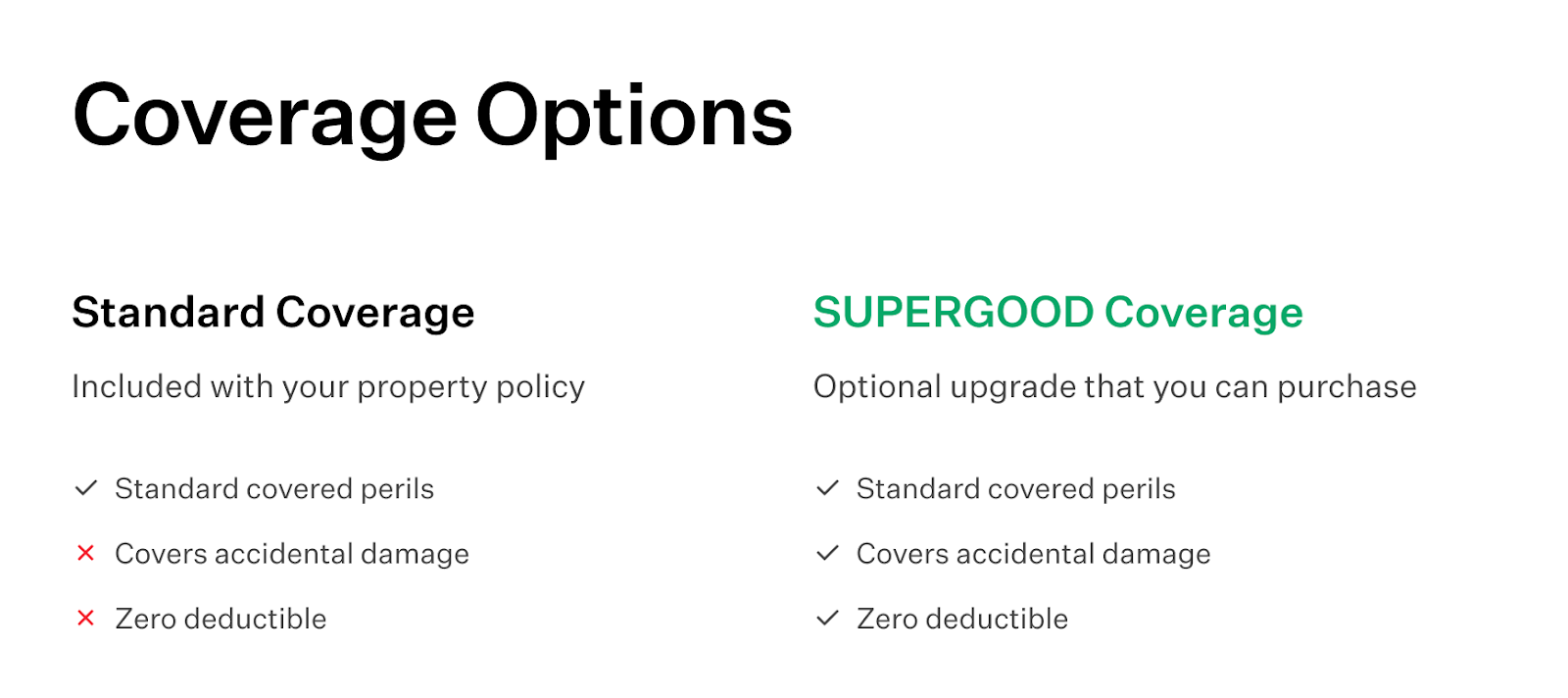

Choose a Renters Insurance Company That Offers Replacement Cost Value

Instead of opting for a renters policy that offers you the actual cash value (ACV) for your personal items, opt for a renters insurance company offering replacement cost value (RCV).

That way, your insurance company will compensate you for all your personal property at market prices (minus the deductible) in case of a covered loss or damage.

Here’s an example:

Let's assume all your personal property, including jewelry, electronics, and furniture worth $20,000, is insured with a deductible of $700 under an insurance provider who pays out ACV.

Now there's a fire in your apartment, and you need to replace all of your personal property. The replacement cost of these items is $20,000, but their depreciated value, or what you could get for the items in used condition, is $10,000. If you have a policy with ACV, you'd be responsible for paying the $700 deductible of the approved claim, and the insurance company would pay the remaining $9,300. Then, you'd also have to pay for the rest of your belongings, worth $10,000, out of your pocket.

With an RCV renters insurance policy like Goodcover’s, you’d have coverage for the full value of replacing your personal property at current market rates, potentially saving you that $10,000 in out-of-pocket expenses.

Increase Your Deductible

Increasing your deductible can reduce your monthly insurance premium payment. A higher deductible means you’ll pay more money out of your pocket before you can use your renters policy, but your monthly payment will be slightly lower.

So, if you have a $500 deductible on an approved $2,000 claim, you’d be responsible for paying $500 — your insurance company would pay the remaining $1,500.

Insurance claims are usually much higher than your deductible, so it’s worth keeping your policy even with a higher deductible.

Switch to a More Affordable Insurance Provider

Consider switching insurance providers instead of canceling your renters policy if you’re feeling the pinch of your premiums.

When shopping for a new policy, compare insurance quotes from multiple insurance providers to get the best deal. For instance, switching to Goodcover could save you up to 71% on your current insurance rates.

Goodcover can handle the cancellation of your policy for you and ensure you stay insured throughout the process if you make the switch.

Additional Perks of Having a Renters Insurance Policy

A renters insurance policy doesn't just cover you against catastrophic events.

Here are some more reasons why you shouldn't cancel your renters insurance policy:

Unexpected Events Won’t Wait Until the Recession Is Over

Let’s say you can no longer live in your rental property due to a covered loss (e.g., a fire). In those cases, renters insurance covers the additional living expenses that come with temporary housing.

Perhaps you move out of your rental to stay with your family to support them during the recession. And you put your belongings in storage. In that case, don’t cancel your renters insurance policy. It covers your personal items even when they are in storage units.

What if you have to temporarily move to another country for work? Don’t worry. Your renters policy will provide worldwide coverage for personal property against theft, damage, and personal liability.

Recession or Not, You’re Still Liable

When someone is injured on your property, you may be found liable. However, certain features in or around your home, known as 'attractive nuisances' (like swimming pools, trampolines, or unfinished construction), can increase your liability risk. These features could attract curious children and potentially lead to injuries. While attractive nuisances are a significant concern, it's crucial for Members to understand that standard renters insurance policies, including ours, may not cover incidents related to these features.

Recognizing how attractive nuisances affect your liability is crucial, especially since the burden of large medical and legal bills could be devastating during a recession.

And ensuring you have appropriate safeguards in place and understanding the specifics of your coverage can help mitigate these risks

Renters Insurance Is Cost-Effective

A renters insurance policy is inexpensive compared to replacing all your personal property or paying someone else's medical bills.

Compare insurance quotes from various insurance companies and select the one offering you the best value. Goodcover plans start at $5 a month. The yearly cost of renters insurance is much cheaper than replacing even a single item of furniture.

A Renters Insurance Policy Can Give You Peace of Mind

Enjoying peace of mind amidst a recession is priceless. Knowing your personal property is covered against unexpected circumstances assures you’ll be able to repair your home and replace personal property.

Final Thoughts: Should You Cancel Renters Insurance During a Recession?

Canceling your renters policy might seem tempting, but being uninsured is risky business.

Instead, consider reaching out to your current insurance provider and asking them to guide you in adjusting your coverage without sacrificing protection.

Goodcover is always happy to help our Members make informed choices about their insurance coverage and ensure they are set up correctly.

Have questions or wish to switch to Goodcover? Get in touch today.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 1 Aug 2024 • 4 min read

Liability Coverage Explained: What Every Renter Needs to Know

Team Goodcover • 26 Jul 2024 • 6 min read

Colorado Renters Insurance: What You Need to Know

Team Goodcover • 6 Jul 2024 • 6 min read

6 Renters Insurance Mistakes (and How to Protect Yourself)

Team Goodcover • 26 Jun 2024 • 8 min read