How Subrogation in Insurance Works and What It Means For You

21 Dec 2023 • 6 min read

If someone else, like your neighbor, causes a mishap that leads to a renters insurance claim — such as a fire from an unattended candle or a water leak that drips down your ceiling — your renters insurance company will attempt to recoup the cost of damage from the at-fault party through a process called subrogation. Subrogation is a fundamental word in the insurance universe, and you might have come across it in your policy documents or heard it during claims settlements.

But even if you’re seeing the term for the first time, subrogation is something that’s helpful to know about. It significantly impacts the insurance claims process, including the financial outcomes for all parties.

This guide will tell you everything you need to know about subrogation in insurance, including what it is, how it works, and, most importantly, its implications for you as a policyholder.

- What Is Subrogation in Insurance?

- Why Is Subrogation Important?

- How Subrogation Works

- Example of Subrogation

- How Long Does Subrogation Take?

- Your Role in the Subrogation Process

- How Subrogation Affects Your Premiums

- What Is a Waiver of Subrogation?

- Final Thoughts: How Subrogation in Insurance Works and What It Means For You

What Is Subrogation in Insurance?

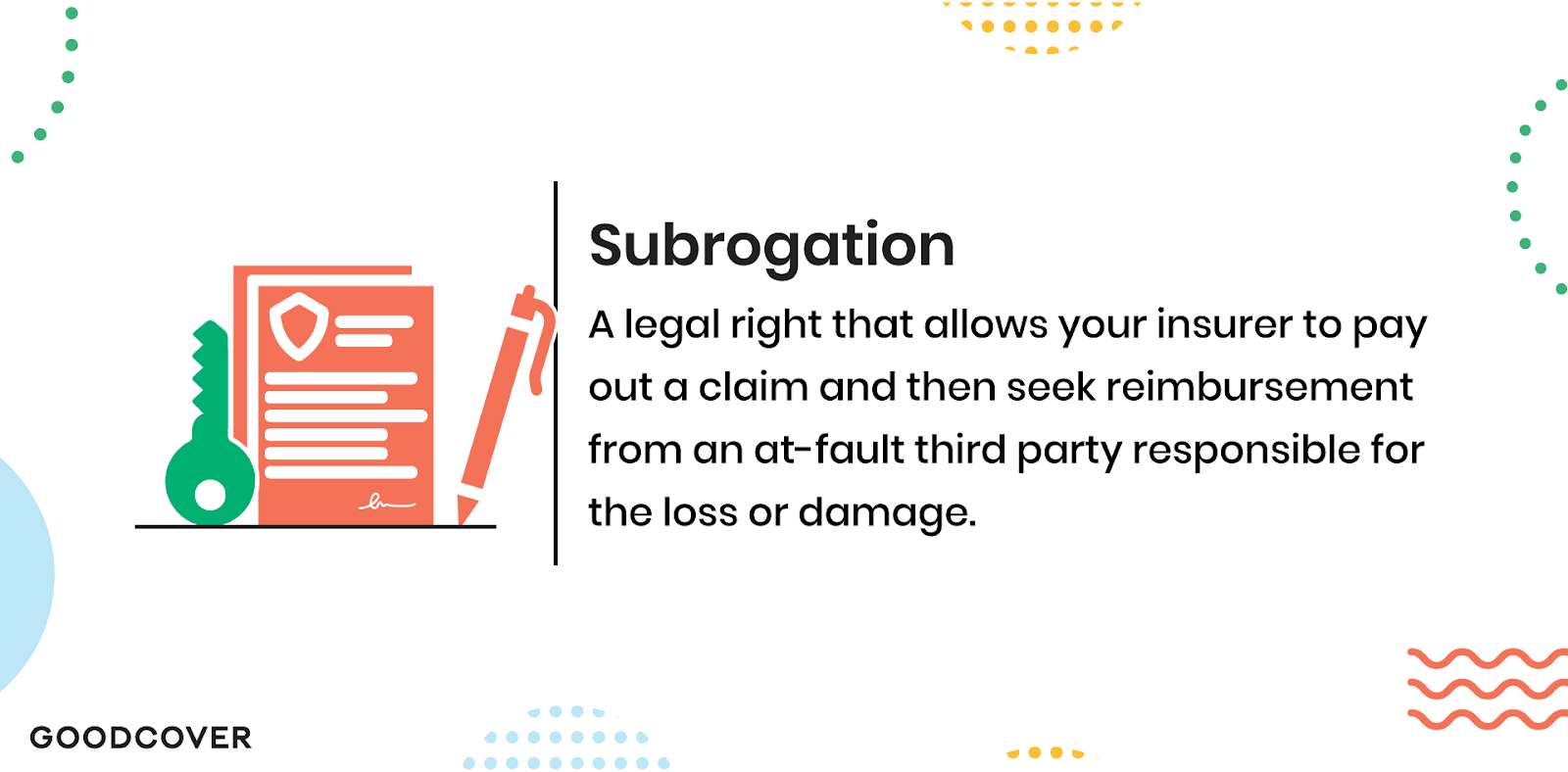

Legally, subrogation is an insurer’s right to pay out a claim and then seek reimbursement from an at-fault third-party responsible for the loss or damage.

This right is typically outlined in your insurance contract, forming a fundamental part of the agreement between you and your insurer.

Subrogation claims are typically made against the at-fault party’s insurance company. But if the person who caused the loss is uninsured, your insurance company may sue the liable party directly.

Subrogation clauses are standard in most insurance contracts, including auto, homeowners, health, and — of course — renters.

Why Is Subrogation Important?

Subrogation in insurance ensures that the financial responsibility for losses or damages rests with the party who is legally liable rather than with the not-at-fault policyholder or their insurance carrier, which helps keep premiums low.

It also helps insurers pay you faster. Since an insurance company pursues recovery from the at-fault party after paying a claim, you receive timely compensation for your loss without the lengthy delays that might happen if your insurer had to wait for the at-fault party to pay first.

For example, you’ve probably seen lawyers advertising big settlements after a car accident. Personal liability lawsuits can take years to settle because of the complexity and amounts involved from medical bills, regardless of whether it is a direct lawsuit, car insurance, or your renters insurance company that are involved.

How Subrogation Works

Insurance companies typically handle the process of subrogation behind the scenes. But it’s still good to know how it works so you know what to expect.

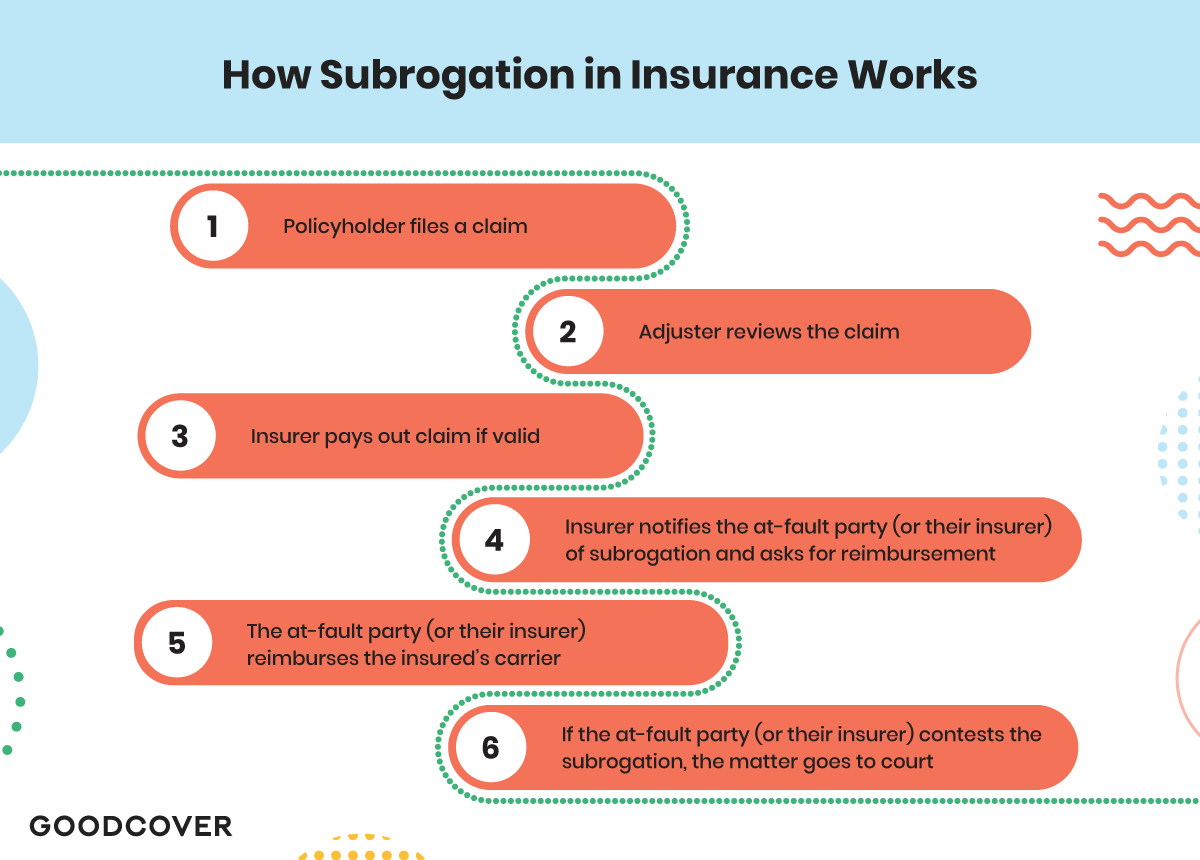

It starts when you file a claim for a loss or damage with your insurance company. The adjuster reviews it and pays out based on your plan’s coverage for a valid claim minus any deductible.

After paying your claim, the insurer gains legal rights to seek reimbursement from the at-fault party — this is the act of subrogation.

Next, your insurer notifies the person at fault (or their insurer) of their intent to recover the funds paid out. This is when they officially request reimbursement.

If the person or their insurer doesn’t fight the subrogation, they reimburse your insurer, and the matter is settled.

Your insurer can sue if the at-fault party, or their carrier, doesn’t pay. Some state laws require your insurer to sue the at-fault person rather than their carrier. In this case, the carrier may provide a lawyer to the at-fault person and then pay any judgment against their insured party up to the policy limits.

In some states like California, the law also requires the at-fault party to pay back at least some of your deductible. Check out the chart below to see the deductible reimbursement law in your state.

Example of Subrogation

Say you filed a claim with your insurer for damages to your television and furniture after your apartment suffered water damage. During the claims process, your insurer discovers that the water damage was due to negligence from your upstairs neighbor, Jerry, who left the water on in his bathtub while he ran to the store.

Rather than delay your payment, your insurer processes your claim and pays you (minus your deductible). Then, your insurer pursues subrogation against Jerry or his renters insurance, seeking reimbursement for the funds paid out to you.

How Long Does Subrogation Take?

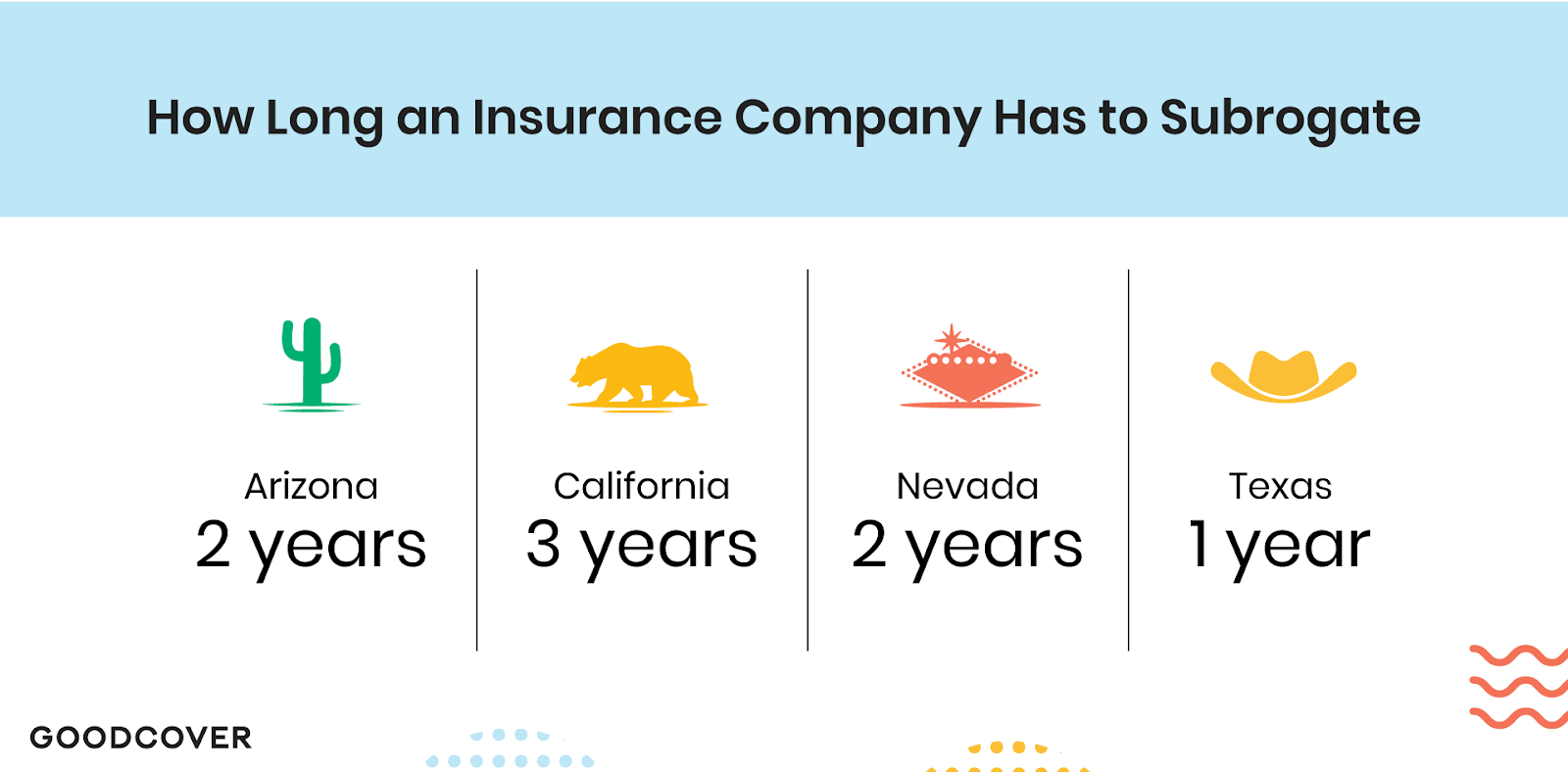

How long an insurer has to subrogate varies by state, but generally gives insurers at least a year to start the subrogation process to allow sufficient time to investigate claims. In the states where Goodcover operates, the timeframe ranges from one to three years.

- Arizona: 2 years

- California: 3 years

- Nevada: 2 years

- Texas: 1 year

The process itself — from filing to full settlement — can take anywhere from a few weeks to over a year, depending on the complexity of the case, the cooperation of the parties involved (or lack thereof), whether it goes to court or not, and the state or jurisdiction where the incident occurred.

In straightforward scenarios, where the at-fault party's insurer readily acknowledges their client's liability, the process is typically quicker.

Conversely, it takes longer if the case involves disputes or legal challenges, such as when someone is injured and medical expenses are involved. But since you’ve already been paid, you don’t have to worry about how long the case may take.

Your Role in the Subrogation Process

As the policyholder, your first role is to promptly report the incident to your insurer, providing all the relevant details and evidence so you can receive compensation.

If your carrier decides to pursue subrogation, cooperate with them during the process. This might include providing extra information and documents or testifying in court if the insurer decides to take legal action.

In most cases, your involvement in the subrogation process will be minimal. Your insurer will do most of the heavy lifting but will update you on the process.

How Subrogation Affects Your Premiums

Subrogation in insurance allows carriers to recover funds from the party responsible for the loss, which helps maintain a lower loss ratio, that is, the number of claims paid compared to premiums received. This keeps down the overall insurance costs for the insurer, which can lead to lower premiums for policyholders.

If you’re a Goodcover Member, you don’t have to worry about any past claims or subrogations.

We believe your premiums should reflect current realities, not past incidents, which are often out of your control, and we don’t penalize you for filing claims. That’s what insurance is for after all.

When you sign up with us, we won’t use any of your past claims against you — including subrogation — when determining your rates.

Other insurance companies aren’t so understanding. If you were at fault for a past claim or had a subrogation issue, you might be classified as high risk, and your premiums would likely increase.

What Is a Waiver of Subrogation?

A subrogation waiver is an agreement where you, as the policyholder, waive your insurer's right to pursue reimbursement from a third party responsible for a loss.

While some insurers may offer this option as a courtesy, when a non-insurer includes them as part of rental or lease agreements, it’s concerning.

Some consider them a red flag of possible problems down the road, as they protect the construction company or landlord and not the tenant or homebuyer.

Waiving the right of subrogation can also affect your current coverage, so we don’t recommend it.

Final Thoughts: How Subrogation in Insurance Works and What It Means For You

Subrogation is more than just a technical term in your insurance policy documents. It's a legal principle with key implications for both you and your insurer. Knowing how it works is a crucial part of understanding your insurance coverage rights and responsibilities.

If you’re in the market for a renters insurance provider to protect your stuff and provide liability coverage in case of a lawsuit, look no further than Goodcover.

Our insurance policies are designed with the modern renter in mind, offering transparency, fairness, and affordability. Get a Goodcover quote today and enjoy the security of insurance that truly has your back.

Note: This post is for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Team Goodcover • 19 Aug 2024 • 10 min read

Colorado Rent Increase Laws: A Comprehensive Guide for Renters

Team Goodcover • 1 Aug 2024 • 4 min read

Liability Coverage Explained: What Every Renter Needs to Know

Team Goodcover • 26 Jul 2024 • 6 min read

Colorado Renters Insurance: What You Need to Know

Team Goodcover • 6 Jul 2024 • 6 min read

6 Renters Insurance Mistakes (and How to Protect Yourself)

Team Goodcover • 26 Jun 2024 • 8 min read