Goodcover’s 2022 Member Dividend Update

6 Oct 2022 • 4 min read

The Goodcover Member Dividend returns any unused premium to our Members at the end of the year – it’s our transparent way of ensuring we’re good stewards of your money.

Every year, we plan to spend 80% of our collected premiums to pay Member claims. We also take a fixed fee of 20% of collected premiums on operating costs. If we spend any less than 80% of your premium on claims, we return what’s left to Goodcover Members via our dividend.

In 2021, we returned 1.93% to eligible Members. In 2020, we returned 1.89%. This year, we expect to need 82.3% of the premiums Members contributed over the last year to pay the claims that have arisen over the same period. That makes this year’s Member Dividend -2.3%.

Essentially, this number means we would have had to collect a little over 2% more premium from each Member to match our expected outcomes. Don’t worry, though; you don’t owe us any money. Let’s discuss how we got to the -2.3% calculation.

How is the Member Dividend calculated?

In September of each year, we begin analyzing how claims, premiums, and expenses fared in comparison to the projections we provided to state insurance regulators. Every year these calculations reveal a different result. There’s never a guarantee that the math will show Goodcover owes refunds to you, but it’s how we demonstrate that we aren’t overcharging you. Our goal is always to get our prediction exactly right and end up with a 0% dividend – so that you’re not overpaying and we’re not overcharging.

Although the Member Dividend is -2.3% this year, we pay the balance out of reserves, and with the help of our insurance capital partners.

Here’s why it cost us more than expected to pay claims this year:

Claim Insights:

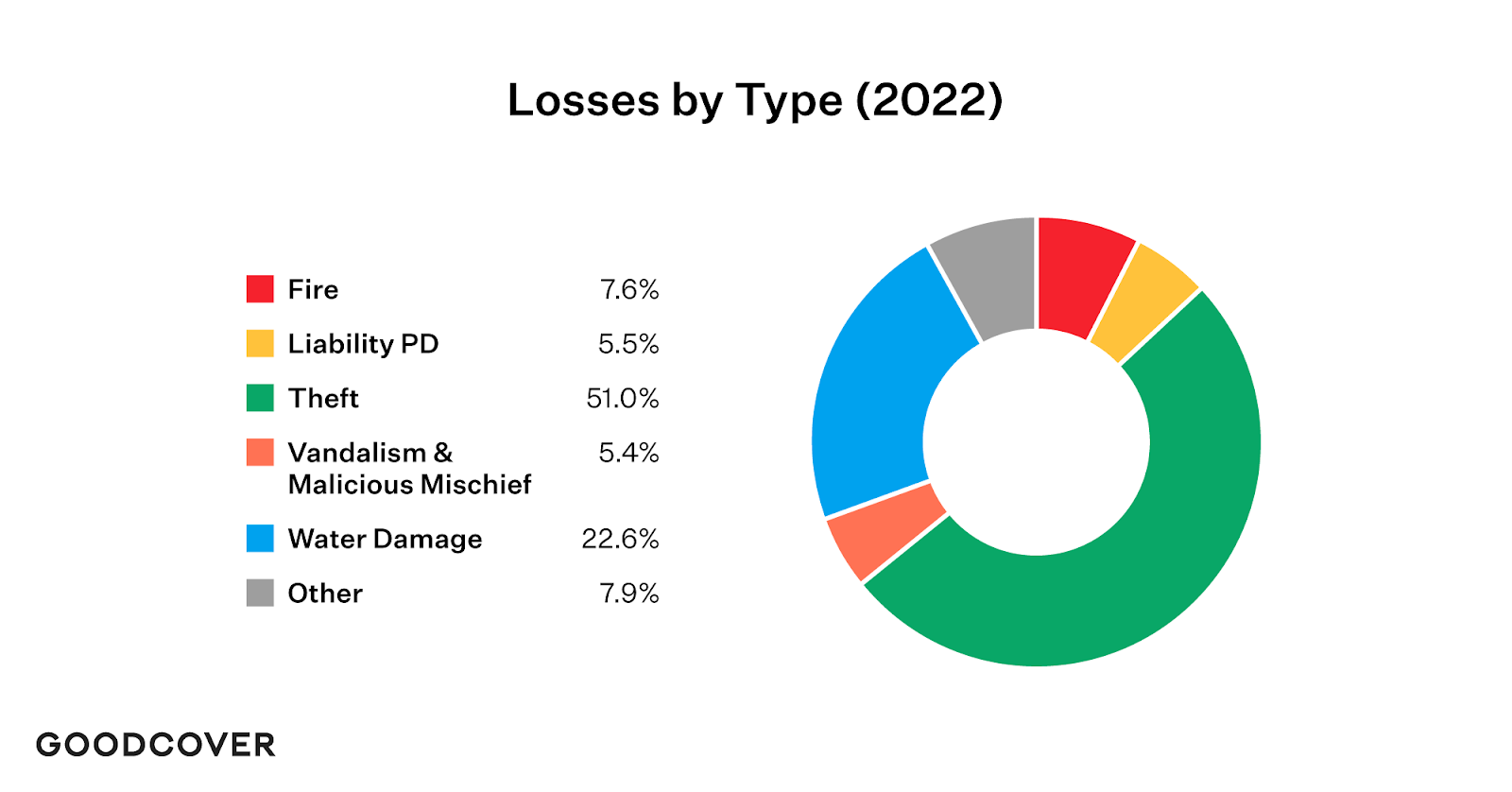

For the third year in a row, theft was the #1 cause of loss. This is normal for Renters Insurance – landlords want you to have a policy because of fire and water damage (which are also sizable causes of loss), but you’re most likely to use Renters Insurance to replace a stolen bike, laptop, or jewelry. In the past year, 51% of claims made and 60% of loss amounts paid were due to theft.

We pay all of our claims at Replacement Cost Value (RCV). That means that when we approve your claim and send a payout, it’s the price you’d pay to replace your item today. In other words, that $1,800 couch you bought in 2016 might cost $2,300 to replace now because of inflation, so we’d pay you $2,300 (subject to your deductible and the individual coverage limits on your policy).

Another significant trend was the gradual increase in each claim payment’s "severity” or average size. This year, the average cost of claims made was 4.74% higher than the year prior. While a 4.74% increase may not seem like much, it is a meaningful amount when it’s balanced against the premiums you’ve contributed to protecting those who’ve suffered losses this year.

Finally, the pandemic resulted in labor shortages, supply chain disruptions, and overall inflation. CBRE estimates that labor and material costs will be up 14.1% year-over-year by the end of 2022. So, if a Member suffered a loss that required construction on the place they rent, it cost us much more money to make those repairs than it would have last year.

These claim insights show why it cost us a bit more to replace your stuff and get your home back in working order this year. More importantly, these insights also imply that you may be underinsured in today’s economy.

What happens next?

Current analysis shows that you may now be underinsured due to inflation and should consider increasing your coverage.

Without making these changes, you may hit your coverage limits quicker than before. If something happens and you don’t update your coverage, you may pay for a future loss out of your own pocket. Yes, even with insurance coverage.

But how much should you adjust?

Since Goodcover is a modern insurance provider, we’ll suggest an increase in coverage that’s right for you. When your renewal period happens, we’ll automatically add an increase in coverage that makes sense based on your current coverage limits and what we’ve learned in the past year from paying claims.

In most cases, you’ll get thousands of dollars in additional coverage with the adjustment, but your premium will only go up a few cents per month. The adjustment we suggest at your renewal is optional; you can make it or opt out completely in your Member Dashboard. You can also make these adjustments yourself at any time, instantly – you don’t need to wait for renewal.

Looking ahead

As we look ahead to 2023, you can rest assured that Goodcover will remain dedicated to fair finance for all – fair risk assessments, fair pricing, and a fair claims process.

We’ll also continue our nationwide expansion. In March, we introduced Texas, Arizona, and Nevada to Goodcover – but we’re not stopping there. Stay tuned for future announcements about where we’re headed next. And if you’re interested in joining the team, check out our open job listings.

From the entire Goodcover team, thank you for trusting us with your Renters Insurance. And thanks for being part of the insurance revolution – your premiums are helping the Goodcover community take care of each other during these difficult times.

CEO and co-founder

More stories

Dan Di Spaltro • 2 Jul 2025 • 16 min read

Affordable Renters Insurance in Sacramento, CA

Team Goodcover • 29 Feb 2024 • 5 min read

Goodcover Reaches New Milestone; Now Serves Half of U.S. Renters

Christopher Lotz • 2 Oct 2023 • 5 min read