7 Losses Your Renters Insurance Doesn’t Cover

13 May 2022 • 5 min read

Moving into your first rental is a big step; you’re finally adulting! As a responsible adult, one of the first things you should do is get renters insurance. Without renters insurance, you and your personal property remain unprotected.

With renters insurance, if someone steals your stuff, you'll have coverage. But it also protects you if someone injures themself in your apartment – you’ll have a personal legal liability to pay their medical bills.

But, don't think that renters insurance will protect you from everything. It won't.

The average millennial or Gen Z renter usually hasn't learned what renters insurance covers and doesn’t cover, and it’s just as important to understand what's not covered to avoid surprises.

With that in mind, let’s avoid these future negative surprises by exploring the range of renters insurance coverage.

What Renters Insurance Doesn’t Cover

- Earthquakes, floods, landslides, or sinkholes

- Car theft

- Costs of moving

- Pet-related incidents

- Some types of water damage

- Property damage

- Impossible-to-Insure Events

Let’s look at these in more detail:

1. Earthquakes, Floods, Landslides, or Sinkholes

Renters insurance doesn’t cover personal property damage caused by earthquakes, floods, landslides, or sinkholes.

Instead, Goodcover rental insurance policies insure you against a broad spectrum of events that might cause damage or loss to your personal property. In the insurance world, these are called covered perils. Covered perils include windstorms, wildfires, water damage, vandalism, and theft, among other losses.

Section I of HO-4 lists 16 named perils, exclusions, and exceptions from coverage. Anything not listed in HO-4 should be insured with other types of policies. For example, you can buy flood insurance to protect your property against flood damage if you live in an area where flooding is common. The same goes for earthquakes. Goodcover offers earthquake insurance through our partner, Palomar.

As a tenant, though, you won’t need to worry about insuring against damage to the building or the property structure because homeowners insurance and landlord insurance covers that.

2. Car Theft

Your car's damage or theft aren't covered events, even if it was parked on your rental property when the damage or theft occurred. Your car insurance policy covers those. However, you’re entitled to reimbursement from Goodcover for the personal items inside the car when the event occurred.

Let’s say someone smashes your car’s window and steals your laptop from the vehicle. The car insurance will cover repairing the window, but Goodcover will likely reimburse you for the computer since it’s your personal property. We’d like your car to also stay protected, so if you’re a Goodcover member but have yet to find fair and affordable auto insurance, check out Goodcover Auto on your Member Dashboard.

3. Moving Costs

Renters insurance doesn’t cover moving costs, except in cases where the rental unit needs repairs due to a covered loss, like if you need to relocate due to water damage in your home.

Renters insurance covers your personal property from covered perils while you move. If property or valuables are damaged or stolen because of you or your moving company's negligence or improper packing, your renters insurance won’t cover such loss. So, make sure you break out the bubble wrap!

When relocation expenses are covered, your renters insurance policy will also cover the additional living expenses you may incur while moving — aka loss of use (temporary housing) coverage.

However, the insurer will usually cap the coverage for the personal property stored away from the rental unit. The cap is typically 10% of the policy’s coverage limit.

4. Pet-Related Incidents

Liability insurance offers liability protection in most cases. However, you should know about exclusions when it comes to pets.

When a pet causes injury, liability coverage on your insurance should protect you.

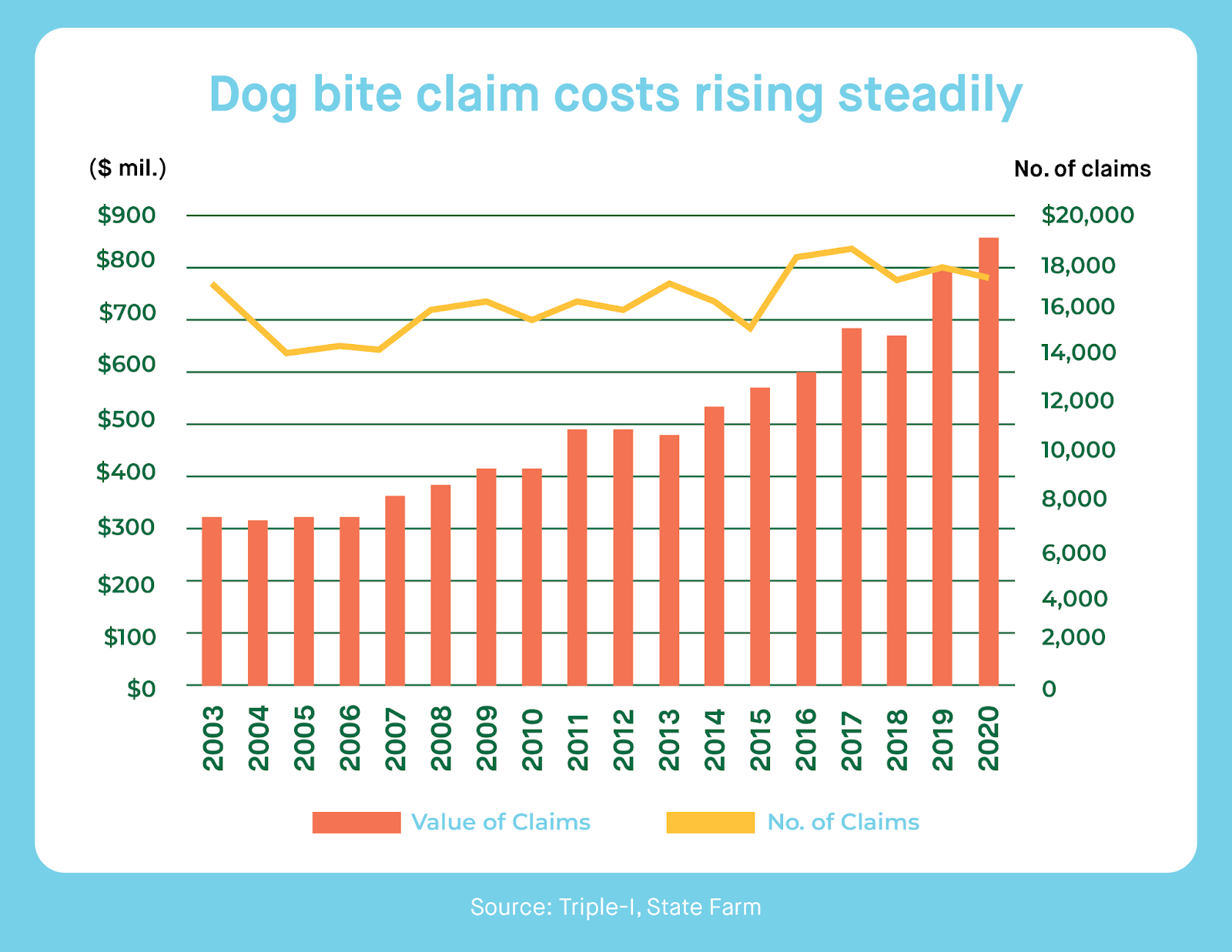

If your dog bites someone, it could cost you an average of $50,245 if the person files a lawsuit to cover their medical bills.

Your renters policy will usually cover such medical expenses and protect you against any liability from the lawsuit. So, what won’t it cover?

You won’t have coverage if the dog is on the vicious dog breed list. Some insurers will even exclude coverage just for owning aggressive breeds.

Plus, renters insurance policies also exclude coverage for exotic pets like monkeys, so you might want to discuss this with your insurance agent.

5. Some Types of Water Damage

Renters insurance doesn’t cover damage caused by leakage from water/sewer backup, but you can get water/sewer backup coverage added for a nominal cost, and sometimes for free.

Your renters insurance policy also won’t cover damage from groundwater coming up because of heavy rains. Your landlord will need to take care of that.

There’s a caveat with coverage for storms. If your landlord hasn’t maintained the property and a storm causes damage, renters insurance won’t cover it. However, the damage would likely be covered if caused by a named peril during a storm, like wind damage.

6. Property Damage

Renters insurance doesn’t cover property damage to your landlord’s housing structure except in specific cases. The landlord should cover any structural damage or wear and tear of the property.

However, if the property is damaged because of a covered loss like fire, your renters insurance will cover that. Plus, renters insurance also covers accidental damage you cause to someone else’s property.

7. Impossible-to-Insure Events

Lastly, certain risks such as wars, nuclear hazards, and government seizures break the math that makes insurance work. These events are so catastrophic and hard to predict that there is no way Goodcover – or any insurance provider – could ever charge enough premium to cover them adequately.

If catastrophes like these occur, implementing federal and state programs will help citizens rebuild. Thankfully, these risks have a relatively low chance of happening and should not concern most renters.

Final Thoughts: What’s Not Covered By Renters Insurance

It’s best to know the types of coverage, coverage limits, and what is not covered by renters insurance to avoid surprises when you finally need to file an insurance claim.

Before you buy renters insurance to protect your possessions, make sure you understand the terms of the policy thoroughly and do your due diligence.

Are you looking for a transparent insurer to insure your personal property? Get a renters insurance quote from Goodcover today.

Note: This post is meant for informational purposes, insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 18 Jul 2025 • 21 min read

Most Affordable Renters Insurance: A Complete Guide

Dan Di Spaltro • 17 Jul 2025 • 18 min read

Affordable Renters Insurance in Florida: Top Picks for Savings

Dan Di Spaltro • 16 Jul 2025 • 22 min read

Your Guide to Affordable Renters Insurance

Dan Di Spaltro • 15 Jul 2025 • 16 min read

Does Renters Insurance Cover Theft? A Simple Guide

Dan Di Spaltro • 14 Jul 2025 • 15 min read